A family life policy is designed to provide financial stability for the people who depend on your income and care, especially when life takes an unexpected turn. When families think about protection, they often focus on the big risks—premature death, serious illness, or a long-term disability that interrupts earnings. Yet the real value of a family life policy is how it transforms uncertainty into a plan: a defined benefit, a clear beneficiary structure, and a predictable framework for paying expenses that do not stop simply because a wage earner is no longer present. Many households carry a mix of obligations that can last decades: rent or mortgage payments, childcare, school costs, car loans, medical bills, and everyday living expenses. A well-chosen family life policy can act as a financial bridge that helps loved ones keep their home, maintain routines, and avoid having to make abrupt, painful decisions during grief. It is not only about replacing income; it is also about preserving choices—time to relocate thoughtfully, time for a surviving spouse to retrain, and time for children to remain in the same school and community.

Table of Contents

- My Personal Experience

- Understanding a Family Life Policy and Why It Matters

- Core Components: Coverage Amount, Term, and Premium Structure

- Aligning a Family Life Policy with Family Goals and Daily Realities

- Term Coverage and Permanent Coverage: Choosing the Right Structure

- How to Estimate the Right Coverage Amount Without Guesswork

- Beneficiaries, Ownership, and Payout Options: Protecting the Right People

- Budgeting for Premiums While Keeping Other Financial Priorities on Track

- Expert Insight

- Health, Age, and Underwriting: How Approval and Pricing Typically Work

- Life Changes That Should Trigger a Review of Your Family Life Policy

- Common Mistakes Families Make and How to Avoid Them

- Building a Broader Protection Plan Around a Family Life Policy

- Choosing a Provider and Keeping the Policy Effective Over Time

- Watch the demonstration video

- Frequently Asked Questions

- Trusted External Sources

My Personal Experience

When my partner and I had our first child, we realized our “family life policy” was basically just good intentions and a shared calendar. After a few rough months of missed dinners and constant last-minute work calls, we sat down on a Sunday night and wrote out a simple set of rules: no emails after 7 p.m., one device-free meal a day, and a rotating schedule for bedtime so neither of us felt like the default parent. We also agreed to talk about money once a month instead of only when we were stressed, and to plan one low-cost family outing every weekend. It wasn’t perfect—there were weeks we slipped—but having something we’d both agreed on made it easier to reset without blaming each other.

Understanding a Family Life Policy and Why It Matters

A family life policy is designed to provide financial stability for the people who depend on your income and care, especially when life takes an unexpected turn. When families think about protection, they often focus on the big risks—premature death, serious illness, or a long-term disability that interrupts earnings. Yet the real value of a family life policy is how it transforms uncertainty into a plan: a defined benefit, a clear beneficiary structure, and a predictable framework for paying expenses that do not stop simply because a wage earner is no longer present. Many households carry a mix of obligations that can last decades: rent or mortgage payments, childcare, school costs, car loans, medical bills, and everyday living expenses. A well-chosen family life policy can act as a financial bridge that helps loved ones keep their home, maintain routines, and avoid having to make abrupt, painful decisions during grief. It is not only about replacing income; it is also about preserving choices—time to relocate thoughtfully, time for a surviving spouse to retrain, and time for children to remain in the same school and community.

Beyond the emotional reassurance, a family life policy can be part of a broader household strategy. Some policies focus on pure protection for a set time period, while others combine protection with features that may accumulate value. For many families, the immediate goal is straightforward: secure adequate coverage at a cost that fits the monthly budget and aligns with responsibilities. But the “right” approach varies based on age, health, number of dependents, debts, and existing savings. A household with young children and a new mortgage typically needs more coverage than a household with grown children and substantial assets. Another factor is how family roles are distributed: if one parent provides most income, the coverage needs may be obvious; if both parents work or if one parent provides unpaid caregiving, the replacement cost of childcare and household management becomes equally important. By understanding how a family life policy functions—coverage amount, term length, premium structure, and beneficiary options—families can choose protection that fits their real life rather than a generic template.

Core Components: Coverage Amount, Term, and Premium Structure

Every family life policy is built from a few fundamental elements that determine how well it matches a household’s needs: the death benefit, the duration of coverage, and the premium. The death benefit is the amount paid to beneficiaries when the insured person dies, and it’s the central figure that should be tied to practical goals. For example, a benefit might be intended to pay off a mortgage, fund several years of living expenses, cover childcare, and set aside money for education. Choosing a benefit amount can be approached using income replacement (such as a multiple of annual earnings) or needs-based planning (adding up specific obligations). Needs-based planning often feels more tangible for families because it converts abstract “coverage” into line items: remaining mortgage balance, estimated monthly bills, health insurance costs, outstanding debts, and expected one-time expenses like funeral costs. The duration of coverage—often called the term—matters because many family obligations are time-bound. If children are young, the highest need may last until they are financially independent; if the family is in the early years of a mortgage, the need may last until the loan is paid down or refinanced into something manageable.

Premium structure determines affordability and long-term sustainability. Some families prioritize the lowest initial premium and accept that the policy may need to be renewed later; others prefer stable premiums over a longer period to avoid surprises. The choice should consider household cash flow and the risk of future insurability. If a parent develops a health condition later, replacing or renewing a policy could become expensive or impossible. That is why many families aim to lock in coverage while they are healthier, even if it means paying slightly more now for stability later. In addition, the premium schedule can be affected by optional add-ons, such as riders for accidental death, waiver of premium in disability, or child coverage. Each add-on changes the cost-benefit equation. A sensible family life policy is not necessarily the cheapest; it is the one the family can keep in force consistently. Lapsed coverage during a tight year can undo years of planning. A strong choice balances sufficient benefit, a realistic term, and a premium that fits alongside other priorities like emergency savings and retirement contributions.

Aligning a Family Life Policy with Family Goals and Daily Realities

A family life policy works best when it is connected to specific goals rather than vague fears. Families often have overlapping aims: keeping children in the same school district, ensuring a surviving spouse can take time off work, paying off a home so housing remains secure, or preventing grandparents from needing to step in financially. The more clearly these goals are defined, the easier it becomes to select a policy structure. For instance, if the primary objective is income replacement for the next 20 years while children are growing up, a time-limited approach may fit. If the objective includes leaving a guaranteed legacy or covering lifelong responsibilities—such as a child with special needs—then long-duration or permanent coverage may be more appropriate. These are not merely financial decisions; they are lifestyle decisions that reflect values, caregiving roles, and the kind of stability a family wants to preserve.

Daily realities also shape what “adequate” means. A household with a stay-at-home parent might assume the working parent is the only one who needs coverage, but the financial impact of losing the primary caregiver can be immense. Childcare, transportation, meal preparation, tutoring, and household coordination have real replacement costs. A family life policy can be used to fund these services so the surviving parent can continue working and maintain routines. Similarly, families with blended structures—shared custody, stepchildren, or obligations to former spouses—benefit from careful beneficiary planning and clear documentation. Another real-world consideration is inflation: expenses like childcare and education often rise faster than general inflation, and medical costs can be unpredictable. Coverage should be reviewed periodically to ensure it still matches the family’s life stage. A policy selected at the birth of a first child might be inadequate after a second child arrives, a larger home is purchased, or a spouse leaves the workforce. Aligning a family life policy with real goals and daily needs turns it from a product into a practical plan.

Term Coverage and Permanent Coverage: Choosing the Right Structure

Families commonly compare time-limited coverage and lifelong coverage, and the best choice depends on how long the financial risk lasts. Time-limited coverage is often selected when the primary need is strongest during certain years: raising children, paying down a mortgage, or building retirement savings. It tends to offer a larger death benefit for a lower premium during the chosen period, which can be attractive for young families balancing childcare, housing, and student loans. A family life policy built on time-limited coverage can be straightforward: choose a term that matches the years of highest dependency, and select a benefit that would cover essential expenses and debts. This structure is often easier to budget for, and it can free up money for emergency funds, retirement accounts, and education savings—other pillars of household resilience.

Lifelong coverage, sometimes referred to as permanent protection, can make sense when there is a desire to guarantee a payout regardless of when death occurs, or when there are lifelong dependents and long-term estate considerations. Some versions may build cash value, which can be accessed under certain conditions, though it is important to understand fees, growth assumptions, and the impact of loans or withdrawals on the death benefit. For a family life policy, permanent coverage can also be used as a tool for leaving an inheritance, equalizing assets among heirs, or covering final expenses so other savings are not depleted. The trade-off is cost: lifelong coverage generally requires higher premiums for the same death benefit. Many households choose a blended strategy, pairing a smaller permanent policy for long-term needs with a larger time-limited policy during the high-responsibility years. The right structure is the one that matches the timeline of obligations, the budget, and the family’s tolerance for complexity.

How to Estimate the Right Coverage Amount Without Guesswork

Estimating coverage for a family life policy becomes easier when the calculation is grounded in a family’s actual balance sheet and monthly cash flow. A practical method starts with immediate obligations: funeral expenses, outstanding medical bills, and any high-interest debts that would be burdensome for survivors. Next, families typically look at housing. If the goal is for the family to remain in the home, coverage may need to pay off the mortgage or provide a fund that covers payments for a set number of years. Then comes income replacement. Instead of choosing an arbitrary multiple, consider how much of the insured person’s income is truly needed to maintain the household’s baseline: utilities, groceries, transportation, insurance premiums, childcare, and school-related costs. Some families aim to cover 60% to 80% of income because certain expenses may decrease, while others aim for close to 100% to preserve stability, especially when childcare and health insurance costs may rise for a surviving spouse.

Education and future milestones are often overlooked. If a household wants to fund college, vocational training, or other education paths, those costs should be estimated realistically, including room and board if relevant. Another overlooked cost is the value of benefits tied to employment, such as health insurance subsidies, retirement matches, or disability coverage. If those benefits disappear, the surviving household may need additional funds to replace them. Families should also consider the role of existing assets: savings, retirement accounts, employer-provided life coverage, and any expected survivor benefits. The goal is not to insure every dollar of future income, but to cover the gap between what survivors will need and what they will already have. A family life policy becomes most effective when it is sized to fill that gap. Finally, it is wise to leave a margin for inflation and unforeseen costs, but not so large that premiums strain the budget and increase the risk of lapsing.

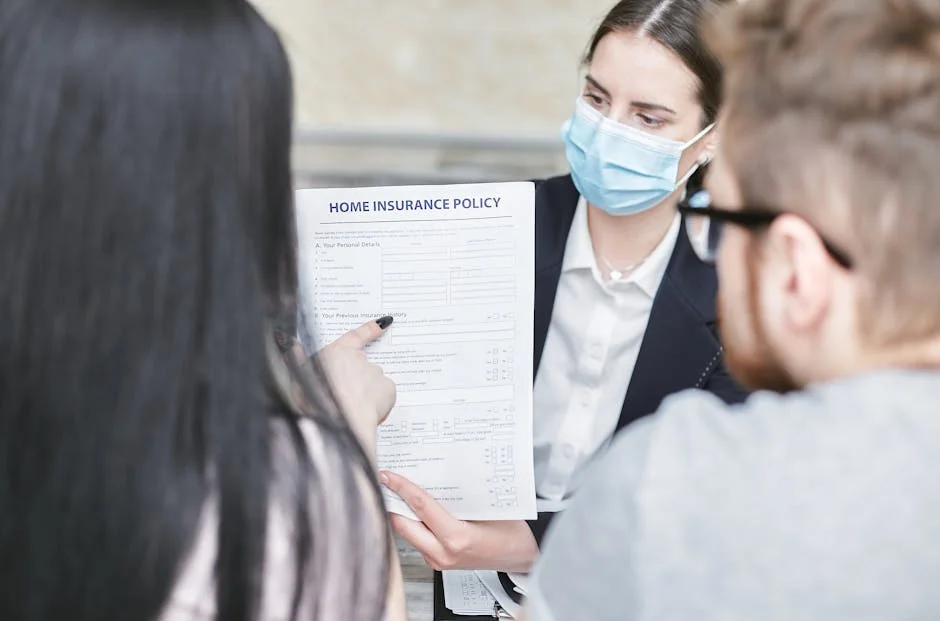

Beneficiaries, Ownership, and Payout Options: Protecting the Right People

A family life policy is only as effective as its beneficiary setup. Naming beneficiaries sounds simple, but family structures can be complex, and small administrative choices can cause major delays or unintended outcomes. Primary and contingent beneficiaries should be designated clearly, with up-to-date names and relationships. For parents of minor children, it is especially important to avoid naming minors directly in a way that could trigger court involvement or require a guardian to manage funds. Many families coordinate life coverage with estate planning tools such as trusts or guardianship arrangements, so the payout supports children in an organized way. Even without complex estate planning, families should at least verify that the beneficiary designations match current intentions after major life events like marriage, divorce, remarriage, or the birth of a child. Beneficiary designations usually override a will, so outdated forms can conflict with what a family believes will happen.

Ownership also matters. The policy owner controls changes, including beneficiary updates and premium payments. In most households, the insured person is also the owner, but there are cases where a spouse or a trust owns the coverage for planning reasons. Payout options can vary as well. Many beneficiaries choose a lump sum for flexibility, but some prefer structured payments to reduce the risk of rapid spending or to mimic a paycheck replacement. This can be particularly useful when the surviving spouse is overwhelmed or when beneficiaries are young adults. Another consideration is coordination with debts and shared obligations. For example, if both spouses contribute to a mortgage, the household might choose coverage for each spouse so that either death does not destabilize the home. A family life policy should be paired with a simple, accessible record-keeping system so beneficiaries know it exists, how to file a claim, and what documents are needed. The best protection is ineffective if survivors cannot locate it quickly.

Budgeting for Premiums While Keeping Other Financial Priorities on Track

A family life policy should strengthen a household’s finances, not crowd out essentials like emergency savings, health coverage, or retirement contributions. The most sustainable approach is to treat premiums as a fixed “protection expense” that fits comfortably within the monthly budget. If premiums are so high that they compete with groceries, childcare, or debt payments, the risk of lapse increases, and the long-term plan becomes fragile. Many families find it helpful to set a target premium range and then adjust term length or benefit amount until the policy fits. The goal is to buy enough coverage to prevent a crisis, not to purchase an idealized amount that becomes unaffordable. For young families, a larger time-limited benefit can often be obtained at a manageable cost, leaving room to build emergency savings and pay down high-interest debt—both of which reduce the need for extremely high coverage later.

| Policy area | What it covers | Typical examples |

|---|---|---|

| Parental leave & caregiving | Time off and job protections for new parents and family caregivers. | Maternity/paternity/parental leave, caregiver leave, phased return-to-work. |

| Childcare & early education | Affordability, availability, and quality standards for childcare and preschool. | Subsidies or tax credits, public pre-K, licensing and staffing ratios. |

| Family income & support | Financial supports that reduce child poverty and stabilize household budgets. | Child benefits, earned income supports, housing assistance, family tax allowances. |

Expert Insight

Start by writing a one-page family life policy that covers the essentials: shared values, weekly routines, screen-time rules, and how decisions get made. Review it together once a month and adjust one rule at a time so changes are clear, realistic, and easy to follow.

Build in accountability with simple systems: a 10-minute weekly check-in to celebrate what worked, name one friction point, and assign one next step to each person. Keep consequences consistent and proportional (loss of a privilege, extra chore, repair action) and always pair them with a clear path to earn trust back. If you’re looking for family life policy, this is your best choice.

It also helps to coordinate coverage with workplace benefits. Many employers provide basic life coverage, but it is often limited to a multiple of salary and may not be portable if employment changes. A family life policy owned privately can provide continuity across job transitions and entrepreneurship. When budgeting, consider the household’s risk profile: a single-income family, a household with a large mortgage, or a family with limited savings may prioritize higher coverage even if it means cutting discretionary spending. Conversely, a dual-income household with strong savings may choose moderate coverage and direct more cash to investments. The best budget decision is one that protects against catastrophic outcomes while keeping progress toward long-term goals. Another practical tip is to pay premiums annually if there is a discount and if cash flow allows, but only after maintaining a solid emergency fund. Ultimately, a family life policy should be viewed as a foundation: it supports everything else by ensuring the household can survive financially even if the worst happens.

Health, Age, and Underwriting: How Approval and Pricing Typically Work

The cost and availability of a family life policy are heavily influenced by underwriting, the process insurers use to assess risk. Age is one of the most significant pricing factors because the likelihood of death generally increases over time. Health history, current conditions, medications, and lifestyle factors such as tobacco use can also affect premiums. Many policies require a health questionnaire, and some require a medical exam or lab tests depending on the coverage amount and the insurer’s rules. Families sometimes delay buying coverage because the process feels intrusive or time-consuming, but waiting can increase costs and introduce the risk of developing a condition that limits options. For households planning to have children, buy a home, or start a business, securing coverage earlier can lock in more favorable rates and reduce future stress.

Underwriting also considers occupation and hobbies. A parent with a high-risk job or dangerous recreational activities may pay more. However, it is important to be accurate and honest in the application. Misstatements can lead to claim disputes or denial. For families, the underwriting process can be approached strategically: gather medical information in advance, understand current prescriptions, and be ready to explain past conditions that are stable or resolved. If one spouse has health issues, it may still be possible to obtain a family life policy with adjusted benefits, alternative insurers, or different policy types. Some families choose to insure both spouses with separate policies to reflect each person’s financial contribution and caregiving role. Others add coverage for children as a small rider or separate policy, typically intended for final expenses and future insurability rather than income replacement. The key is to treat underwriting as a normal part of building a reliable plan. A policy that is issued at a fair, sustainable premium becomes a long-term asset to the household’s stability.

Life Changes That Should Trigger a Review of Your Family Life Policy

A family life policy should not be set and forgotten, because family life evolves. Certain events should prompt a coverage review to ensure the benefit amount, term length, and beneficiaries still align with reality. The birth or adoption of a child is a major trigger because dependency increases and childcare costs often rise. Marriage or remarriage changes legal and financial responsibilities, while divorce may require updating beneficiaries, ownership, and obligations such as child support. Buying a home, refinancing a mortgage, or taking on significant new debt can increase the need for coverage, especially if the household relies on one income to keep housing stable. Career changes also matter. A promotion could increase lifestyle costs and expectations, while a transition to self-employment could remove employer-provided benefits and create new risks.

Health changes can also justify a review, even if the policy is already in force. If a family member develops a condition that might make future coverage more expensive, it may be wise to secure additional protection sooner rather than later, provided the budget allows. On the other hand, if a household accumulates substantial savings, pays off debt, and approaches a stage where children are financially independent, it may be possible to reduce coverage or allow a time-limited policy to expire without replacement. Another often overlooked trigger is a move to a new state or country, which can affect legal considerations and access to certain products. Families should also revisit their plan after the death of a beneficiary, the creation of a trust, or changes in guardianship preferences. A family life policy is most effective when it stays synchronized with the household’s actual responsibilities. A brief annual review—checking beneficiaries, confirming premium payments, and reassessing major debts—can prevent painful surprises later.

Common Mistakes Families Make and How to Avoid Them

One common mistake is underinsuring because the household focuses only on current bills rather than future needs. Families may think, “We could cut expenses if something happened,” without recognizing that grief and disruption often increase costs in the short term. Childcare may become more expensive, a surviving spouse may need time off work, and support services may be needed to keep life functioning. Another mistake is relying solely on employer-provided coverage, which may be insufficient and may disappear with a job change. A family life policy owned privately can provide consistency across employment shifts and protect the household even during periods of unemployment or career transition. A related error is choosing a policy term that is too short. If coverage ends while children are still dependent or the mortgage is still large, the family may face higher costs to renew later, especially if health has changed.

Administrative oversights can be just as damaging as financial ones. Outdated beneficiaries are a frequent problem, especially after divorce or remarriage. Another issue is failing to communicate the existence of the policy. If the surviving spouse or trusted family member cannot find policy documents, they may not know which insurer to contact, and claims can be delayed. Premium lapses are also common when families change bank accounts, move, or experience temporary financial stress. Setting up automatic payments and keeping contact details current with the insurer can reduce this risk. Some families also misunderstand cash value features, assuming they function like a savings account without realizing that withdrawals or loans can reduce the death benefit and may create tax consequences. Avoiding these mistakes is mostly about clarity: choose coverage that matches real obligations, keep the plan simple enough to maintain, update beneficiaries promptly, and store documents where survivors can access them. A family life policy is meant to reduce stress, so the best approach is the one that remains dependable through life’s changes.

Building a Broader Protection Plan Around a Family Life Policy

A family life policy is a cornerstone, but it works best when paired with other forms of protection that address different risks. Disability coverage is a major complement because the loss of income due to illness or injury is more common than premature death during working years. If a parent becomes unable to work, the household may face years of reduced earnings, medical costs, and caregiving expenses. Health insurance, emergency savings, and a realistic budget also support the policy’s purpose by reducing the chance that the family will be forced into debt or lapse coverage. Liability protection, such as adequate auto and homeowners or renters insurance, reduces the risk that a lawsuit or accident will drain savings that were meant to support children and long-term goals. For families with dependents, guardianship planning and basic estate documents can ensure that money is managed responsibly and that children are cared for by the people the parents trust.

Coordination is what turns separate products into a coherent plan. For example, if a household maintains a strong emergency fund, it may be able to choose a slightly lower death benefit because short-term expenses are already covered. If the family has significant retirement savings, the coverage goal may shift from income replacement to paying off the mortgage and funding education. Conversely, if savings are minimal and debt is high, a larger family life policy may be essential to prevent survivors from facing immediate financial hardship. Another aspect of coordination is timing: many families prioritize life coverage during high-dependency years, then gradually shift focus toward retirement funding as children become independent and debts decline. The policy should be revisited alongside these shifts. When protection tools work together, the family is less likely to rely on a single payout to solve every problem. A family life policy remains the central safety net, but the net is stronger when the household also builds savings, maintains appropriate insurance, and keeps legal documents aligned with real-life intentions.

Choosing a Provider and Keeping the Policy Effective Over Time

Selecting a provider for a family life policy is not only about price; it is also about reliability, clarity, and service. Families benefit from insurers with a strong track record of paying claims and providing straightforward policy management tools. Policy language should be understandable, and the process for updating beneficiaries or changing addresses should be simple. It is wise to compare quotes for similar coverage and to pay attention to the details that affect long-term value: renewal terms, conversion options, exclusions, and how premiums may change over time. Some families prefer working with a licensed agent who can explain trade-offs; others prefer direct-to-consumer options that may feel more streamlined. Either way, the household should keep copies of the application, the policy contract, and any riders, and confirm that beneficiaries are accurate. Small details, like a misspelled name or an outdated address, can create unnecessary delays during a claim.

Keeping the policy effective is a matter of maintenance. Premiums should be paid on time, and the insurer should have current contact information. Families should store policy information in a secure but accessible place and tell at least one trusted person where to find it. A yearly check-in can confirm that the family life policy still matches the household’s structure and obligations. If the family has expanded, taken on new debt, or experienced income changes, it may be time to adjust coverage. If the family has paid off major debts and built substantial assets, the coverage need may be lower or may shift toward different goals. The final measure of success is simple: if something happens, will the surviving family members have the money and the clarity they need to continue life with dignity and options? When chosen thoughtfully, maintained carefully, and aligned with real responsibilities, a family life policy delivers exactly that kind of stability—quiet, practical protection that supports the people you love when they need it most.

Watch the demonstration video

In this video, you’ll learn what family life policy is and why it matters for everyday households. It explains how policies can support families through childcare, parental leave, healthcare, and work–life balance, and how these decisions affect children’s wellbeing, parents’ opportunities, and family stability in the long term.

Summary

In summary, “family life policy” is a crucial topic that deserves thoughtful consideration. We hope this article has provided you with a comprehensive understanding to help you make better decisions.

Frequently Asked Questions

What is a family life policy?

A family life policy is a set of guidelines that defines expectations and support for employees’ family-related needs, such as parental leave, caregiving, flexible work, and family benefits.

Who is covered under the family life policy?

Coverage usually starts with employees and can also extend to spouses or partners, children, and other eligible dependents, depending on your organization’s rules under its **family life policy**.

What types of leave are usually included?

Common types of leave include maternity, paternity, and parental leave; time off for adoption or foster placement; family caregiving leave; bereavement leave; and leave for unexpected family emergencies—all often outlined in a company’s **family life policy**.

Does the policy support flexible work arrangements?

Many roles offer a **family life policy** with options such as flexible working hours, remote or hybrid arrangements, reduced schedules, and phased returns after leave—depending on job requirements and with manager approval.

How do I request family-related leave or accommodations?

Employees typically submit their requests through HR or the company’s leave management system, providing any required documentation and giving the appropriate notice. The **family life policy** clearly explains the approval process and the steps you’ll need to follow.

How does the policy protect privacy and prevent discrimination?

A strong **family life policy** helps protect sensitive information by clearly defining who can access it, sets out straightforward confidentiality practices, and makes it explicit that retaliation or discrimination—whether related to pregnancy, parental status, or caregiving responsibilities—will not be tolerated.

📢 Looking for more info about family life policy? Follow Our Site for updates and tips!

Trusted External Sources

- Family Life Insurance – State Farm®

Family insurance, simplified. Instead of juggling multiple plans, you can protect your immediate family with one straightforward **family life policy**—all under a single rate and one easy-to-manage plan.

- Family Life Insurance Company – ManhattanLife

Family Life Insurance Company specializes in mortgage protection life insurance, helping safeguard what matters most—your family’s home—through a trusted **family life policy** designed to keep them secure if the unexpected happens.

- Individual & Family Life Insurance | Employee Benefits

As of May 29, 2026, Individual & Family Life Insurance (I&F) provides term life coverage for you, your spouse or domestic partner, and eligible children—making it easier to protect the people who matter most with a family life policy.

- Life Insurance for Families | Aflac

This article will explain how life insurance for families works, including costs, types, and tips on getting a policy.

- Life Insurance (Voluntary and Family) – City of Milwaukee

Life insurance options—basic, voluntary, and family—are administered through the Employees’ Retirement System (ERS), which manages the group coverage available to members. If you’re reviewing your benefits, be sure to check how the **family life policy** works, what it covers, and whether it fits your household’s needs.