Choosing a credit card without balance transfer fee can feel like finding a loophole in an industry built on small print, but the value is straightforward: it removes one of the biggest upfront costs of moving debt from one card to another. Many balance transfer offers advertise a low or even 0% introductory APR, yet still charge a transfer fee that’s commonly 3% to 5% of the amount moved. On a $10,000 transfer, that can mean $300 to $500 added instantly—before a single dollar of principal is paid down. When the goal is to get out of revolving debt faster, that extra cost can slow progress, especially if the new promotional APR is short or if the monthly payment plan is tight. A no-fee transfer offer reduces the “break-even” time, meaning you start saving interest sooner and can direct more of each payment to the balance itself rather than recouping a fee.

Table of Contents

- My Personal Experience

- Understanding a credit card without balance transfer fee and why it matters

- How balance transfer fees work and what “no fee” really means

- Who benefits most from a no-fee balance transfer offer

- Key features to compare beyond the missing transfer fee

- How to calculate savings with a credit card without balance transfer fee

- Qualifying factors: credit score, income, and debt-to-income considerations

- Common pitfalls: deferred interest confusion, purchases, and payment allocation

- Expert Insight

- Step-by-step strategy to use a no-fee balance transfer effectively

- When a no-fee transfer card may not be the best option

- How to find and evaluate offers without getting trapped by marketing

- Building a payoff plan that lasts beyond the promotional period

- Final thoughts on choosing a credit card without balance transfer fee

- Watch the demonstration video

- Frequently Asked Questions

- Trusted External Sources

My Personal Experience

When I realized I was paying more in fees than I was knocking off my debt, I started looking for a credit card without a balance transfer fee. My old card charged a percentage just to move the balance, which felt like getting penalized for trying to do the right thing. I found a card that let me transfer what I owed without that upfront cost, and it made an immediate difference—my first payment actually went toward the principal instead of disappearing into a transfer charge. It didn’t magically fix my spending habits, but it gave me a cleaner starting point and a clearer payoff timeline, which honestly made it easier to stay disciplined. If you’re looking for credit card without balance transfer fee, this is your best choice.

Understanding a credit card without balance transfer fee and why it matters

Choosing a credit card without balance transfer fee can feel like finding a loophole in an industry built on small print, but the value is straightforward: it removes one of the biggest upfront costs of moving debt from one card to another. Many balance transfer offers advertise a low or even 0% introductory APR, yet still charge a transfer fee that’s commonly 3% to 5% of the amount moved. On a $10,000 transfer, that can mean $300 to $500 added instantly—before a single dollar of principal is paid down. When the goal is to get out of revolving debt faster, that extra cost can slow progress, especially if the new promotional APR is short or if the monthly payment plan is tight. A no-fee transfer offer reduces the “break-even” time, meaning you start saving interest sooner and can direct more of each payment to the balance itself rather than recouping a fee.

A credit card without balance transfer fee is most useful when you already have high-interest balances and a clear payoff plan. The fee you avoid is effectively a guaranteed return, because it’s a cost you don’t pay at all. That said, the overall deal still depends on the introductory APR, the length of the promo period, and the ongoing APR after the promotion ends. Some no-fee transfer cards offset the missing fee by offering a shorter 0% window, a higher post-promo APR, or fewer perks. Others reserve the no-fee benefit for specific transfer types, such as transfers made within a narrow time frame after account opening, or transfers coming from particular issuers. Understanding these details matters because the most affordable option isn’t always the one with the biggest headline promise; it’s the one that matches your timeline, your monthly budget, and your ability to avoid new debt while you pay down what you already owe.

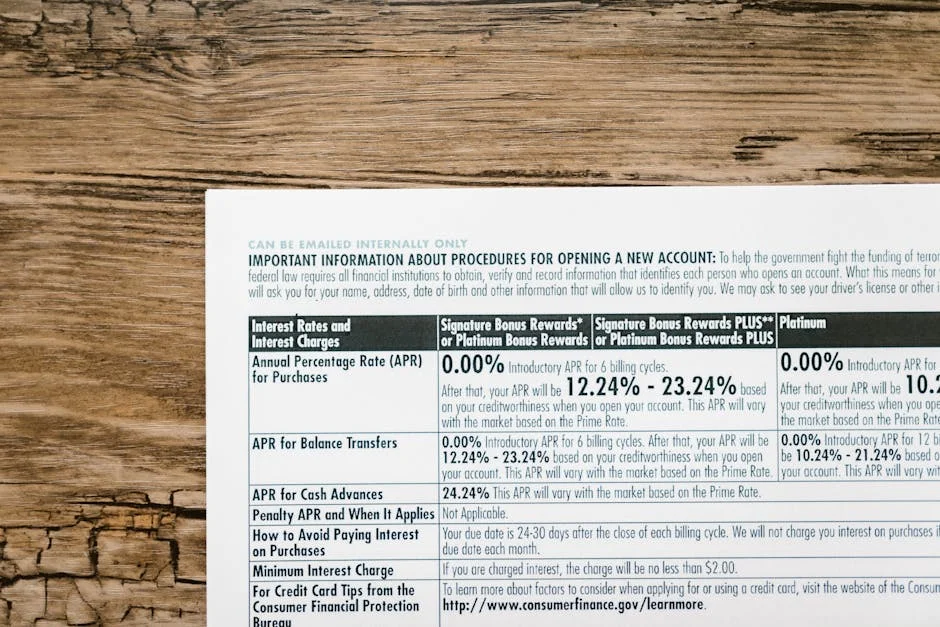

How balance transfer fees work and what “no fee” really means

Balance transfer fees are typically calculated as a percentage of the amount you move, often with a minimum dollar charge. A common structure is 3% to 5% of the transferred balance, with a minimum fee of $5 to $10. This means transferring $500 might still cost $10 even if 3% would be $15, and transferring $20,000 could cost $600 to $1,000 depending on the issuer. That fee is usually added to your new card balance immediately, which can matter if your card has a maximum transfer limit or if you’re trying to keep utilization lower for credit score reasons. When you see a credit card without balance transfer fee, it generally means the issuer is waiving this charge—at least under stated conditions—so the amount you move is the amount you owe, not the amount plus a surcharge.

However, “no fee” can be conditional. Some offers waive the fee only for transfers completed within the first 30 to 60 days of account opening. Others waive the fee for transfers from a specific issuer group, or they might waive it only for a promotional period and then apply a fee to later transfers. It’s also important to distinguish between “no balance transfer fee” and “no annual fee”; they’re separate. A card can have no transfer fee but charge an annual fee, and that annual fee could reduce the savings you expected—especially if you’re planning to keep the card only for a year. Reading the pricing and terms section is the practical way to confirm: look for “Balance Transfer Fee: $0” and check whether it includes timing language such as “for transfers made within X days.” If the wording is unclear, it’s safer to assume the waiver has limits and plan your transfer quickly to capture the full benefit. If you’re looking for credit card without balance transfer fee, this is your best choice.

Who benefits most from a no-fee balance transfer offer

A credit card without balance transfer fee tends to benefit people with larger balances, because percentage-based fees scale up quickly. If you’re transferring $2,000, a 3% fee is $60—still meaningful, but it might be outweighed by a longer 0% period on a card that does charge a fee. If you’re transferring $15,000, the same 3% fee becomes $450, which can be hard to justify if you can qualify for a truly no-fee option. People who are close to paying off their balances can also benefit, because they may not have enough months of interest savings to “earn back” a fee before the promotional APR ends. In those cases, avoiding the fee can make the transfer worthwhile even if the intro APR period is modest.

Borrowers who are disciplined about not adding new charges to the card also gain more from a no-fee transfer. Many issuers apply payments to the lowest APR balance first, which means if you start making purchases on the card, those purchases might accrue interest while your transferred balance sits at 0%. A no-fee transfer card is not a cure-all; it’s a tool that works best when paired with a payoff schedule and spending boundaries. If you can commit to paying a fixed amount monthly, avoid new revolving debt, and finish repayment within the promotional period, the no-fee structure maximizes the portion of your payment that reduces principal. That is the central advantage: your money goes to your debt, not to an upfront transaction cost. If you’re looking for credit card without balance transfer fee, this is your best choice.

Key features to compare beyond the missing transfer fee

Even when you find a credit card without balance transfer fee, comparing the rest of the terms is essential. The introductory APR length is often the biggest driver of total cost. A 0% APR for 12 months versus 18 months can change your monthly payment requirement significantly. For example, a $9,000 balance would require $750 per month to clear in 12 months, but $500 per month over 18 months—before considering any remaining interest. If your budget can’t support the higher payment, you could end the promo period with a leftover balance that starts accruing interest at the regular APR, which might be high. The best no-fee transfer offer is the one that gives you enough time to pay down the balance at a realistic monthly pace.

Also compare the regular APR range, because life happens and payoff plans can slip. If you end up carrying a balance after the promotional period, a lower ongoing APR can reduce damage. Check whether the card has an annual fee, late payment fees, foreign transaction fees, and penalty APR policies. Some issuers apply a penalty APR after late payments, which can make remaining balances more expensive. Credit limits matter too: your approval limit may not cover the entire amount you want to move, and some issuers cap transfers at a percentage of the credit line. Finally, consider whether the card offers tools like free credit score tracking, autopay discounts (rare), or hardship programs. While these aren’t as flashy as a fee waiver, they can support consistent repayment and protect you from costly mistakes. If you’re looking for credit card without balance transfer fee, this is your best choice.

How to calculate savings with a credit card without balance transfer fee

To estimate savings, start with the fee you would have paid on a typical transfer card. If your alternative option charges 3% and you’re moving $8,000, the fee would be $240. A credit card without balance transfer fee saves that $240 immediately. Next, calculate interest savings from the promotional APR. If your current card charges 24% APR and you’re paying down slowly, interest can be significant. Roughly, 24% APR is about 2% per month (it varies by compounding method), meaning an $8,000 balance could accrue around $160 in interest in the first month alone if you’re not paying aggressively. Moving that balance to 0% can free up cash flow so more of your payment reduces principal. The combination of avoided transfer fee plus avoided interest is the real value.

But it’s important to compare two offers realistically. Suppose Card A is a no-fee transfer card with 0% for 12 months, and Card B charges a 3% fee but offers 0% for 18 months. If you can pay off in 12 months, Card A likely wins because you avoid both interest and the fee. If you can only afford payments that clear the balance in 16 or 18 months, Card B might be cheaper overall even with the fee, because the longer 0% window prevents interest after month 12. The clean way to compare is to map your monthly payment plan and see whether you’ll carry a balance past the promo end date. A no-fee transfer is most powerful when it aligns with a payoff horizon you can actually meet, not one you hope you can meet. If you’re looking for credit card without balance transfer fee, this is your best choice.

Qualifying factors: credit score, income, and debt-to-income considerations

Approval for a credit card without balance transfer fee often requires good to excellent credit, though there are exceptions depending on the issuer and the specific product. Issuers evaluate your credit score, payment history, utilization, recent inquiries, and the mix and age of accounts. If you’ve had late payments, maxed-out cards, or multiple recent applications, you may still be approved but with a lower credit limit, which can restrict how much you can transfer. Income and debt-to-income ratio matter as well, because the issuer wants to see capacity to repay. Even if you plan to pay the transferred balance aggressively, the bank relies on underwriting models that consider overall risk, not your intentions.

If your credit is borderline, improving your profile before applying can increase your odds of landing a no-fee transfer offer. Paying down current balances to reduce utilization can help quickly, as can correcting errors on your credit report. Avoid applying for multiple cards in a short span, because inquiries and new accounts can reduce your score temporarily. If you’re self-employed or have variable income, be prepared to document income accurately; issuers may verify. Also consider that some issuers allow prequalification checks that don’t affect your score, which can offer a hint about your likelihood of approval. The best outcome is not only getting approved, but getting a credit line high enough to make the transfer meaningful and to keep utilization reasonable after the move. If you’re looking for credit card without balance transfer fee, this is your best choice.

Common pitfalls: deferred interest confusion, purchases, and payment allocation

One reason people seek a credit card without balance transfer fee is to keep the math simple and avoid hidden costs. Still, pitfalls remain. First, confirm that the offer is truly a 0% introductory APR and not a deferred interest promotion (more common with store financing than general credit cards). With deferred interest, if you don’t pay the entire balance by the end of the period, you may owe interest retroactively from the start. Most mainstream balance transfer cards use intro APR rather than deferred interest, but it’s worth verifying the wording. Second, avoid using the new card for purchases unless you understand how payments are applied. If your transferred balance is at 0% and purchases are at the regular APR, your payments may go to the 0% portion first, leaving purchase interest to accumulate.

| Option | Balance Transfer Fee | Best For |

|---|---|---|

| True no-fee balance transfer card | 0% (no balance transfer fee) | Moving a large balance without paying an upfront transfer cost |

| Intro 0% APR card with a transfer fee | Typically 3%–5% (often a minimum fee applies) | Paying down debt interest-free during the promo period when the fee is outweighed by interest savings |

| Low ongoing APR card (no/short promo) | Varies by issuer; may still charge 3%–5% | Carrying a balance longer-term after the promo ends or if you won’t qualify for top 0% offers |

Expert Insight

Compare credit cards without a balance transfer fee by calculating the total payoff cost: prioritize a long 0% intro APR window, then check the post-intro APR and any annual fee to ensure the savings aren’t offset elsewhere. If you’re looking for credit card without balance transfer fee, this is your best choice.

Before applying, confirm the transfer timeline and limits: ask how long you have to complete the transfer to qualify for the promo rate, verify eligible debt types, and set a payoff plan that clears the balance before the intro period ends. If you’re looking for credit card without balance transfer fee, this is your best choice.

Late payments are another major risk. Many issuers will end a promotional APR if you pay late, and some may apply a penalty APR. That can turn a smart strategy into a costly one quickly. Autopay for at least the minimum payment is an effective safety measure, and paying more than the minimum is critical if your goal is to eliminate debt within the promo window. Also watch for balance transfer limits and timing requirements. If the no-fee condition applies only within the first 60 days, procrastinating can accidentally trigger a fee later. Finally, don’t ignore how the transfer affects your old card. If you keep it open, you might be tempted to run up balances again; if you close it, you might reduce available credit and potentially impact utilization. The healthiest approach is to treat the transfer as a structured repayment project and prevent new revolving debt from replacing the old. If you’re looking for credit card without balance transfer fee, this is your best choice.

Step-by-step strategy to use a no-fee balance transfer effectively

Using a credit card without balance transfer fee effectively starts before you apply. First, list the balances you want to move, their APRs, and their minimum payments. Then decide the maximum monthly amount you can commit to debt repayment without relying on future income increases. This monthly number should guide your selection of intro APR length. Next, check your credit reports for errors and pay down any small balances that are inflating utilization. When you apply, aim for one strong application rather than several. If you’re approved, initiate the balance transfer immediately to meet any “within X days” requirement for the fee waiver. Keep proof of the offer terms and the date you requested the transfer, and monitor both accounts until the transfer posts and the old balance is reduced.

Once the transfer is complete, set up autopay for at least the minimum payment, then schedule additional payments aligned with your payoff timeline. A practical method is to divide the transferred amount by the number of promo months and pay that amount each month, adding a buffer if possible. For example, if you transfer $6,000 and have 12 months at 0%, paying $520 per month rather than $500 builds slack for months when expenses spike. Avoid new purchases on the transfer card, and if you must use it, pay those charges off immediately so they don’t accrue interest. On the old card, consider keeping it open but inactive, especially if it has no annual fee and a long history, because that can support your credit profile. The core idea is that a no-fee transfer removes one barrier, but the payoff still depends on consistent execution month after month. If you’re looking for credit card without balance transfer fee, this is your best choice.

When a no-fee transfer card may not be the best option

A credit card without balance transfer fee is not automatically the cheapest solution for every situation. If you can’t qualify for a strong intro APR length, or if the credit limit offered is too low, the benefit may be limited. Also, if a competing card charges a fee but offers a significantly longer 0% period, the longer runway can be worth more than the upfront cost—especially when the alternative is paying regular APR after a shorter promo ends. Another scenario is when your debt is so large or your budget so constrained that you’re unlikely to pay it down within any promotional window. In that case, a structured installment loan, a credit counseling debt management plan, or negotiating APR reductions with current issuers could produce more predictable results.

There are also behavioral considerations. If transferring the balance gives a false sense of progress and leads to new spending, the strategy can backfire, leaving you with multiple balances instead of one. Additionally, some no-fee transfer cards may have fewer consumer-friendly features, such as weaker dispute resolution tools, fewer account alerts, or stricter penalty terms. If you travel internationally, foreign transaction fees might matter more than the transfer fee you saved. And if you anticipate needing to transfer again later, remember that many issuers restrict repeat promotional offers or apply fees to subsequent transfers. The best choice is the one that reduces your total cost while also fitting your habits and financial stability, not just the one that advertises the most appealing single feature. If you’re looking for credit card without balance transfer fee, this is your best choice.

How to find and evaluate offers without getting trapped by marketing

Finding a credit card without balance transfer fee requires filtering offers carefully, because many promotions emphasize 0% APR while downplaying the fee. Start by scanning the card’s pricing and terms section, not just the marketing headline. Look specifically for a line item labeled “Balance Transfer Fee.” If it states $0, confirm whether it includes timing conditions. If it lists a percentage but mentions a temporary waiver, note the deadline and any limitations. Also verify whether the 0% APR applies to balance transfers, purchases, or both, and whether the promotional periods differ. Some cards offer 0% on purchases for longer than transfers, which might not help if your main goal is debt consolidation.

Next, evaluate the issuer’s reputation for customer service, the clarity of statements, and the ease of setting up autopay and alerts. Those operational details matter when you’re using a transfer as a payoff tool, because a missed due date can erase savings quickly. Consider whether the card allows you to choose a payment due date that matches your cash flow cycle. If you’re transferring multiple balances, check whether the issuer can send payments to multiple creditors and whether there are restrictions on transferring from cards issued by the same bank. Finally, compare at least two or three realistic alternatives, including one that charges a fee but offers a longer 0% period, so you can make a decision based on total payoff cost rather than a single waived charge. If you’re looking for credit card without balance transfer fee, this is your best choice.

Building a payoff plan that lasts beyond the promotional period

The strongest reason to choose a credit card without balance transfer fee is to accelerate repayment, but the plan should account for what happens after the promotional APR ends. If you can pay the balance to zero within the intro period, your job is mostly about consistency. If you might carry a remainder, you need an “endgame” plan: either increase payments before the promo ends, save a lump sum to apply near the end, or prepare to refinance again only if it makes financial sense. Relying on another transfer later can be risky, because future approval is not guaranteed and fees or terms may change. A good payoff plan treats the promotional period as a deadline, not as an invitation to delay.

Practical tactics include setting a monthly target that ensures payoff at least one month early, tracking progress with a simple spreadsheet, and using windfalls like tax refunds or bonuses to reduce principal. If you’re juggling multiple debts, consider whether you’ll keep paying minimums on other accounts while focusing on the transferred balance, or whether you’ll transfer multiple balances to simplify. Either way, avoid letting the old cards fill back up. If spending control is a challenge, it may help to move to a cash-first budget for day-to-day expenses while you’re in payoff mode. The goal is to make the no-fee transfer a one-time pivot point that reduces interest costs and creates momentum, rather than a temporary shuffle that postpones the real work of paying down the debt. If you’re looking for credit card without balance transfer fee, this is your best choice.

Final thoughts on choosing a credit card without balance transfer fee

A credit card without balance transfer fee can be a high-impact way to cut the cost of debt repayment, especially when you have a clear timeline and the discipline to avoid new balances. The missing fee can save hundreds of dollars upfront, and when paired with a solid introductory APR, it can turn months of interest payments into months of principal reduction. The smartest approach is to confirm the waiver conditions, choose an intro period that matches your budget, automate payments to avoid mistakes, and treat the promotional window as a firm payoff deadline. When those pieces fit together, a credit card without balance transfer fee becomes less of a promotional gimmick and more of a practical tool for getting out of revolving debt efficiently.

Watch the demonstration video

In this video, you’ll learn how to find a credit card with no balance transfer fee and when it can actually save you money. We’ll cover key terms to watch for, common hidden costs, and how to compare offers so you can pay down debt faster and avoid unnecessary interest and charges. If you’re looking for credit card without balance transfer fee, this is your best choice.

Summary

In summary, “credit card without balance transfer fee” is a crucial topic that deserves thoughtful consideration. We hope this article has provided you with a comprehensive understanding to help you make better decisions.

Frequently Asked Questions

What is a credit card with no balance transfer fee?

A **credit card without balance transfer fee** lets you move debt from another card without paying a transfer charge—often $0—at least for a limited promotional period.

Do no-fee balance transfer cards still charge interest?

Many cards come with a 0% introductory APR on balance transfers for a limited period, giving you time to pay down what you owe before the standard APR kicks in on any remaining balance—especially if you choose a **credit card without balance transfer fee**.

Are there limits on how much I can transfer with no fee?

Yes—you can, but there are limits. How much you’re able to move depends on your approved credit limit and the issuer’s balance transfer cap (often set as a percentage of that limit), even if you’re using a **credit card without balance transfer fee**.

How long does a balance transfer take to complete?

Most balance transfers take about 5–14 days to process, though some may take longer. Until the transfer officially posts, continue making payments on your current card so you don’t get hit with late fees or extra interest—especially if you’re using a **credit card without balance transfer fee** to save even more.

Can I transfer a balance between cards from the same bank?

In most cases, no—card issuers typically won’t let you transfer a balance from one of their cards to another, even if the cards are different products or carry different brand names. If you’re trying to cut costs, it may be worth looking for a **credit card without balance transfer fee** from a different issuer instead.

What should I watch out for with a no-fee balance transfer offer?

Review how long the intro APR lasts, when the no-fee period expires, any minimum amount required to transfer, and whether purchases are charged interest under different terms—especially if you’re choosing a **credit card without balance transfer fee**.

📢 Looking for more info about credit card without balance transfer fee? Follow Our Site for updates and tips!

Trusted External Sources

- Are there any cards with zero fees for balance transfers? – Reddit

Sep 30, 2026 … No, there are no cards that offer 0% Balance Transfer and $0 fee to do so. Best rate is 3%. That amount gets added to your debt and in pretty … If you’re looking for credit card without balance transfer fee, this is your best choice.

- What are Credit Cards with No Balance Transfer Fees – Citi.com

As of Oct 7, 2026, some issuers offer introductory balance transfer promotions that waive the usual transfer charge—so you can shift existing debt to a **credit card without balance transfer fee** and avoid paying the typical percentage-based cost upfront.

- Are there credit cards with no balance transfer fee? – Reddit

Dec 5, 2026 … We always do 0 apr cards. Gf and I are going on vacation in February and she has a card with 0 apr till July so instead of getting a new card … If you’re looking for credit card without balance transfer fee, this is your best choice.

- Low Rate Credit Card | No Balance Transfer Fee – BECU

0% Intro APR for your first 12 months on purchases, and 0% intro APR on balance transfers if processed within the first 90 days of account opening, after rates … If you’re looking for credit card without balance transfer fee, this is your best choice.

- Low Intro APR on Balance Transfers to a Platinum Card

WalletHub® recently recognized Navy Federal Credit Union’s Platinum credit card as one of the Best Credit Cards With No Balance Transfer Fees for 2026—an appealing option for anyone looking for a **credit card without balance transfer fee** and a straightforward way to manage existing debt.