0 interest and balance transfer credit cards are built around a simple promise: for a limited time, you can carry a balance at a promotional APR that is typically 0% on purchases, transferred balances, or both. That limited time is the entire point, because the value comes from what you do during the intro period. When used with a plan, these offers can reduce how much of your monthly payment is eaten by interest, allowing more money to go toward principal. When used without structure, the same product can quietly become expensive after the promotion ends, especially if the ongoing APR is high or if fees and penalties apply. The best approach is to treat the promotional window like a deadline, not a discount, and to set a payoff target that fits inside the intro term. A card’s marketing may emphasize “0%,” but the real decision factors include intro length, transfer fee, regular APR, penalty APR triggers, and whether the issuer applies payments in a way that benefits you.

Table of Contents

- My Personal Experience

- Understanding 0 interest and balance transfer credit cards

- How promotional APR periods work in real life

- Balance transfer basics: what can be moved and what cannot

- Interest savings math: fees, intro length, and payoff speed

- Credit score considerations and application impacts

- Choosing the right card features beyond the 0% offer

- Common mistakes that make promotional offers expensive

- Expert Insight

- Strategies to pay off transferred debt before the intro period ends

- When 0% purchase offers make sense alongside transfers

- Comparing balance transfers to personal loans and other options

- How to apply, transfer, and manage the account smoothly

- Long-term habits to avoid repeating the debt cycle

- Final thoughts on using promotional credit wisely

- Watch the demonstration video

- Frequently Asked Questions

- Trusted External Sources

My Personal Experience

I signed up for a 0% interest balance transfer card after realizing my old credit card was barely making a dent in the debt because the interest kept piling on. The transfer itself was straightforward, but the 3% transfer fee stung a little—still, it was worth it to stop the monthly interest charges. I set up automatic payments and divided the balance by the number of 0% months so I’d actually finish before the promo ended, and I avoided using the new card for purchases since those can start accruing interest right away. About halfway through, I almost missed a payment when I switched banks, and it hit me how easy it would be to lose the promo rate over one mistake. By the time the 0% period was close to ending, my balance was down to a manageable amount, and having a clear payoff timeline felt way less stressful than just “paying what I could” each month. If you’re looking for 0 interest and balance transfer credit cards, this is your best choice.

Understanding 0 interest and balance transfer credit cards

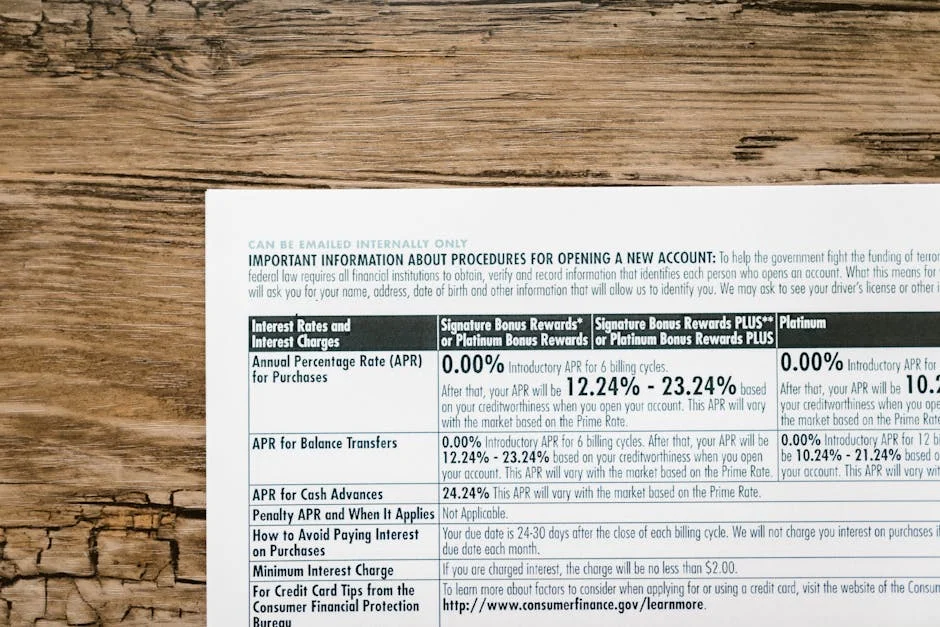

0 interest and balance transfer credit cards are built around a simple promise: for a limited time, you can carry a balance at a promotional APR that is typically 0% on purchases, transferred balances, or both. That limited time is the entire point, because the value comes from what you do during the intro period. When used with a plan, these offers can reduce how much of your monthly payment is eaten by interest, allowing more money to go toward principal. When used without structure, the same product can quietly become expensive after the promotion ends, especially if the ongoing APR is high or if fees and penalties apply. The best approach is to treat the promotional window like a deadline, not a discount, and to set a payoff target that fits inside the intro term. A card’s marketing may emphasize “0%,” but the real decision factors include intro length, transfer fee, regular APR, penalty APR triggers, and whether the issuer applies payments in a way that benefits you.

Many consumers seek 0 interest and balance transfer credit cards because they want to consolidate multiple high-interest debts into a single monthly payment. Others want to finance a large planned purchase without paying interest while they pay it off. In both cases, the product is a tool, not a solution by itself. The tool works best when you know the exact balances, the minimum payments, the date the promotion ends, and the total cost of moving debt. A promotional rate does not erase debt; it changes the math of repayment. A common misunderstanding is that a 0% offer means “no cost,” but balance transfers often have a fee, usually a percentage of the amount moved. Another misunderstanding is that you can transfer any type of debt; most issuers restrict transfers from the same bank family and may not accept certain obligations. Understanding the mechanics helps you avoid disappointment and prevents a short-term strategy from turning into a long-term problem.

How promotional APR periods work in real life

Promotional APRs are governed by the card’s terms and the issuer’s policies, and those details can dramatically change outcomes. Intro periods typically start when the account is opened, not when you first use the card, so delaying action can waste valuable months. For balance transfers, many issuers require that the transfer be completed within a set window—often the first 60 to 120 days—to qualify for the promotional rate. If you transfer after that window, the balance may accrue interest at the standard APR immediately. For purchases, the 0% purchase APR usually applies to new purchases made during the intro period, but it may not apply to cash advances, convenience checks, or certain quasi-cash transactions. When the promotional period ends, any remaining balance begins accruing interest at the ongoing APR, and the interest cost can rise quickly if the balance is still large. If you’re looking for 0 interest and balance transfer credit cards, this is your best choice.

Payment allocation is another real-world factor that can influence your results. If you have a balance transfer at 0% and purchases at a different rate (or vice versa), issuers often apply payments above the minimum to the highest APR balance first, as required by law in many situations. However, the minimum payment can still be applied in ways that leave you with a lingering balance at the end of the promotion. Additionally, some cards offer 0% on purchases but not on transfers, or 0% on transfers but not on purchases. Mixing transactions without a plan can create multiple “buckets” with different APRs and different end dates. That complexity is why many people choose to use one card strictly for the transfer and avoid new spending on it. The clearer and simpler the transaction pattern, the easier it is to pay everything off before the promotional APR expires. If you’re looking for 0 interest and balance transfer credit cards, this is your best choice.

Balance transfer basics: what can be moved and what cannot

A balance transfer typically means moving existing credit card debt from one issuer to another, with the new card paying the old creditor and creating a new balance on your new account. Some issuers also allow transfers of personal loan balances, medical bills, or other debts, but those cases often require special handling or may be processed as a cash advance, which is usually excluded from 0% offers. Transfers between cards issued by the same bank are commonly restricted; even if the card brands differ, the underlying issuer relationship matters. This is important when comparing 0 interest and balance transfer credit cards because the “best” offer is not helpful if it cannot accept your current debt. It’s also important to understand that a transfer does not reduce your total debt; it changes who you owe and how interest is calculated.

Timing and logistics can also affect your cost. Balance transfers can take several days to a few weeks to post, and during that time your old card may still require a payment to avoid late fees. If you stop paying the old card too soon, you may trigger penalties and credit score damage even though you initiated the transfer. Another common issue is transferring an amount close to the new card’s credit limit; if the issuer approves a lower limit than expected, you may not be able to move the full balance, leaving you with multiple payments and interest charges. Some issuers offer direct transfers to creditors, while others provide convenience checks. Convenience checks may not qualify for the promotional APR or may be treated differently, so reading the fine print is essential. A strong strategy includes keeping your old account current until the transfer is confirmed, then verifying that the old balance is paid and that no residual interest or trailing charges remain. If you’re looking for 0 interest and balance transfer credit cards, this is your best choice.

Interest savings math: fees, intro length, and payoff speed

The value of 0 interest and balance transfer credit cards can be estimated with straightforward math. Start with your current APRs and balances, then estimate how much interest you would pay if you continued making your planned payments without a transfer. Next, compare that to the cost of the transfer fee and any interest you might pay if you do not finish repayment before the intro period ends. A balance transfer fee is commonly 3% to 5% of the amount transferred, so moving $10,000 might cost $300 to $500 upfront. That fee can still be worth it if your current APR is high and you can pay down the balance aggressively during the promotional period. However, if you only plan to make minimum payments, the fee may not be offset by the reduced interest, and you could end the intro period with most of the balance still intact.

Intro length matters because it determines how large your monthly payment must be to reach a zero balance in time. For example, a 15-month promotional term requires larger payments than a 21-month term for the same balance. Yet a longer term is not always better if the transfer fee is higher or if the card’s regular APR is especially steep. Another consideration is whether the card offers 0% on purchases as well; if you plan a major expense, a purchase intro offer can be useful, but only if you avoid adding new debt that prevents payoff of the transferred balance. Many people find that the best results come from a strict payoff plan: divide the transferred balance plus the fee by the number of months in the promotional window, then set that as an automated payment. The math becomes even more favorable when you stop adding new spending and redirect “freed up” interest savings into principal reduction. If you’re looking for 0 interest and balance transfer credit cards, this is your best choice.

Credit score considerations and application impacts

Applying for 0 interest and balance transfer credit cards typically results in a hard inquiry, which can cause a small, temporary dip in your credit score. More significant, though, is how the new account changes your credit utilization and your average age of accounts. If the new card comes with a high credit limit, it can lower your overall utilization once balances are transferred and paid down, which may help your score over time. But if you transfer a large balance and immediately use most of the new limit, utilization on that specific card may be high, and that can offset some benefits. Another factor is that opening a new account can reduce your average account age, which may slightly hurt your score in the short term. These effects vary by credit profile, but they are worth considering if you plan to apply for a mortgage, auto loan, or other major financing soon.

Closing old cards after transferring balances is a common question. Keeping older accounts open can preserve available credit and account age, which can support your score, but only if you can manage them responsibly and avoid new debt. If a card has an annual fee that is no longer worth paying, closing it might be reasonable, but it should be weighed against utilization changes. Another potential pitfall is that some people transfer a balance, feel relief, and then run up the old card again, ending up with more total debt. The score impact can then worsen because utilization rises across multiple accounts. A disciplined approach is to keep the old account open, set it to a low-use pattern or lock it away, and focus on paying off the transferred balance within the promotional period. If you are rebuilding credit, it can also help to avoid multiple applications within a short time, since several inquiries can signal risk to lenders. If you’re looking for 0 interest and balance transfer credit cards, this is your best choice.

Choosing the right card features beyond the 0% offer

Not all 0 interest and balance transfer credit cards are equally useful, even if the headline promotional APR looks identical. The intro period length for transfers and purchases may differ, and the transfer fee can vary. Some cards offer a lower fee for transfers made within the first few days, then raise it afterward, while others set a single fee. Also, consider whether the card has an annual fee. Paying an annual fee can still be worthwhile if the promotional savings are large, but many consumers prefer no annual fee options to keep costs predictable. Another feature to review is the standard APR after the intro period. If there is any chance the balance will remain, a lower ongoing APR can reduce the downside risk. Penalty APR policies also matter; a single late payment might trigger a significantly higher APR, which can erase much of the benefit of the promotion.

Rewards and perks are often less important for a dedicated transfer strategy, but they can still matter if you plan to keep the card long term. Some cards offer rewards on purchases, but using the same account for spending can complicate payoff because new purchases may not have a grace period when you carry a balance. If the card offers 0% on purchases, the temptation to spend can undermine the repayment plan. Another practical feature is the issuer’s online tools: clear statements, autopay options, and alerts for due dates can prevent costly mistakes. Customer service and dispute handling can matter too, especially if you are transferring large balances and want accurate posting and confirmation. The best selection process involves matching features to your specific goals: debt consolidation, planned purchase financing, or a mix, while keeping the structure simple enough that you can execute the plan without confusion. If you’re looking for 0 interest and balance transfer credit cards, this is your best choice.

Common mistakes that make promotional offers expensive

The most frequent mistake with 0 interest and balance transfer credit cards is treating the promotional APR as permission to delay repayment. When people only pay the minimum, the balance barely moves, and the remaining debt becomes subject to the regular APR after the intro period. Another mistake is missing a payment. Even one late payment can lead to late fees, loss of the promotional rate, or a penalty APR depending on the card’s terms. Autopay for at least the minimum payment is a basic safeguard, but it does not replace a payoff plan. Also, some cardholders transfer balances and then continue spending on their old cards, effectively increasing total debt. The relief from lower interest is real, but it must be paired with behavior changes if the goal is to get out of debt rather than reshuffle it.

Expert Insight

Before applying for a 0% interest or balance transfer card, map out a payoff timeline that fits within the promotional period and set up automatic payments above the minimum. This helps you clear the balance before the regular APR kicks in and reduces the risk of losing the promo rate due to a missed payment. If you’re looking for 0 interest and balance transfer credit cards, this is your best choice.

Compare balance transfer fees, promo length, and any deferred-interest terms, then transfer only what you can realistically pay off on time. Keep new purchases off the card (or choose a card with a separate 0% purchase offer) to avoid complicating payments and potentially accruing interest on new charges. If you’re looking for 0 interest and balance transfer credit cards, this is your best choice.

Another costly error is misunderstanding what qualifies for the 0% rate. Cash advances, wire transfers, lottery purchases, and similar transactions may be excluded or treated as cash-like, often accruing interest immediately at a high APR plus fees. Convenience checks can fall into this category, so relying on them without confirming the terms can backfire. Additionally, some people transfer a balance that is near the credit limit and then get hit with over-limit issues if fees push the balance beyond the limit or if the issuer adjusts the limit. It is also easy to overlook the “transfer posting” timeline and end up paying interest and fees on the old card because a payment was missed while waiting for the transfer to complete. Finally, applying for multiple cards to chase longer promotional windows can create complexity and increase the risk of missed payments, while also adding inquiries and new accounts that may affect credit. A single well-chosen card and a clear payoff schedule often beat a complicated multi-card approach. If you’re looking for 0 interest and balance transfer credit cards, this is your best choice.

Strategies to pay off transferred debt before the intro period ends

A reliable payoff strategy starts with a precise target. Take the transfer amount, add the balance transfer fee, then divide by the number of months in the promotional period. That figure is your baseline monthly payment to reach zero by the deadline. If your budget allows, rounding up creates a buffer for timing issues, residual interest on the old card, or small statement variances. Many people set autopay for the calculated amount, not just the minimum, and then monitor statements monthly to confirm progress. If you receive extra income—bonuses, tax refunds, or side gig earnings—applying it to the balance can shorten the payoff timeline and reduce the risk of carrying debt past the promotional window. Keeping the card dedicated to repayment, with no new purchases, keeps the math clean and reduces the chance of payment allocation surprises. If you’re looking for 0 interest and balance transfer credit cards, this is your best choice.

| Feature | 0% Intro APR Purchase Cards | 0% Balance Transfer Cards | 0% Purchase + Balance Transfer Cards |

|---|---|---|---|

| Best for | Financing new purchases over time without interest during the intro period | Paying down existing high-interest debt faster by moving it to a 0% intro APR offer | Covering both upcoming purchases and existing debt with one card (with careful planning) |

| Key costs & terms to check | Length of 0% intro APR on purchases, ongoing APR after the promo ends | Balance transfer fee, intro APR length on transfers, transfer window/deadline | Separate promo periods for purchases vs. transfers, fees, and how payments are applied |

| Common pitfalls | Carrying a balance past the promo period and paying a higher regular APR | Missing the transfer deadline, transferring too much, or not reducing the balance before the promo ends | Mixing purchases with transferred debt can complicate payoff; interest may accrue sooner if not managed |

Budget structure matters as much as the card terms. A practical approach is to freeze discretionary spending categories temporarily and redirect that money to the payoff plan. Another approach is the “debt snowflake” method: small savings from daily decisions are accumulated weekly and added as extra payments. If you are consolidating multiple cards, consider keeping the old accounts open but removing them from digital wallets and turning off stored payment methods to reduce impulse spending. It can also help to set calendar reminders for the promo end date 60 and 30 days in advance, giving you time to adjust payments if needed. If you realize you cannot finish repayment on time, planning ahead is still valuable: you may be able to increase payments, explore a lower-APR personal loan, or consider a second transfer only if it truly reduces total cost and you can manage the added complexity. The core principle is simple: the promotional period is a runway, and the payoff plan is the takeoff. If you’re looking for 0 interest and balance transfer credit cards, this is your best choice.

When 0% purchase offers make sense alongside transfers

Some 0 interest and balance transfer credit cards include 0% on purchases as well as transfers, and that combination can be helpful in specific situations. For example, someone consolidating debt might also need to replace a broken appliance or cover a planned expense that would otherwise go on a high-interest card. A 0% purchase APR can reduce interest costs, but only if the total balances remain manageable and you can still meet the payoff timeline. The danger is that new purchases can slow debt repayment by increasing the total balance you must eliminate before the promo ends. Even if both transfers and purchases are at 0%, the total amount is what matters. If you add spending, your required monthly payment rises, and the plan can become unrealistic. That is why many people use a dedicated 0% purchase card for planned expenses and a separate transfer card for consolidation, but that adds complexity and requires strong payment discipline.

Another subtle issue is the loss of the grace period on new purchases when you carry a balance. With many cards, if you carry any balance from month to month, new purchases may start accruing interest immediately unless they are also covered by a 0% purchase promotion. If the purchase promotion ends earlier than the transfer promotion, you can end up with purchases accruing interest while the transfer is still at 0%, complicating payment allocation. A safer approach is to avoid new purchases on the transfer card entirely unless you are sure the purchases are included in the 0% term and you can track the end dates. If you do use the card for purchases, consider paying purchases off quickly to keep the balance from ballooning. The best use of 0% purchase offers is intentional, planned, and time-bound, not a way to maintain a lifestyle while hoping the promotional period will somehow solve the underlying budget gap. If you’re looking for 0 interest and balance transfer credit cards, this is your best choice.

Comparing balance transfers to personal loans and other options

0 interest and balance transfer credit cards compete with personal loans, debt management plans, and other consolidation methods. A personal loan offers fixed payments and a fixed payoff date, which can be easier to manage psychologically and logistically. It can also avoid the risk of a high APR after a promotional period ends. However, personal loan rates depend heavily on creditworthiness, and they may not beat a 0% intro offer in total cost if you can pay the balance within the promotional window. Balance transfers can be cheaper in the short run but require more discipline, since the minimum payment structure can encourage slow repayment. Another difference is that personal loans typically do not have variable APR changes due to missed payments in the same way credit cards do, though late fees and credit reporting consequences still apply.

Debt management plans through reputable credit counseling agencies can reduce interest rates and consolidate payments, but they may require closing cards and following structured repayment terms. That can be a good fit for someone who needs guardrails and wants to avoid new credit use. Home equity products may offer lower rates but put your home at risk, making them unsuitable for many households. Retirement account loans or withdrawals can have long-term opportunity costs and tax consequences. The best comparison comes down to your timeline and behavior: if you can commit to an aggressive payoff and avoid new debt, 0 interest and balance transfer credit cards may be the lowest-cost path. If you need a longer payoff horizon or want predictable fixed payments, a personal loan or structured program may be safer, even if the interest rate is higher than 0% for a limited time. Choosing the right tool is less about the headline rate and more about what you can reliably execute month after month.

How to apply, transfer, and manage the account smoothly

The application process for 0 interest and balance transfer credit cards is straightforward, but preparation reduces surprises. Before applying, gather your current balances, account numbers, and payoff goals. Check your credit reports for errors, since inaccuracies can affect approval and credit limit decisions. When you apply, the issuer may offer instant approval or may require verification. If approved, note the exact promotional terms, including the intro length, the transfer deadline, and the transfer fee. Once you receive the card, initiate the balance transfer promptly to maximize the promotional period. Some issuers allow you to request transfers during the application; others require you to wait until you have the account number. Keep records of the transfer requests, including confirmation numbers and dates, and continue paying at least the minimum on old accounts until the transfer is fully posted and the old balance shows as paid.

After the transfer posts, set up autopay for more than the minimum payment, ideally the amount that ensures payoff before the intro period ends. Track the promotional end date and consider setting alerts 60 days before it expires. Also, monitor statements for any interest charges that should not be there; sometimes interest appears due to transaction categorization or timing, and it is easier to resolve quickly. Avoid cash advances and avoid using the card for purchases unless you are intentionally using a 0% purchase promotion and can manage the additional balance. If you plan to keep the card long term, evaluate whether the ongoing APR and benefits justify continued use after the balance is paid. Some cardholders switch the card to a low-utilization, on-time payment pattern to support credit history, while others prefer to simplify and use a different everyday card. Smooth management is about consistency: on-time payments, minimal complexity, and a clear finish line. If you’re looking for 0 interest and balance transfer credit cards, this is your best choice.

Long-term habits to avoid repeating the debt cycle

Successfully using 0 interest and balance transfer credit cards can be a turning point, but only if the underlying habits change. Many people fall back into debt because the transfer creates temporary breathing room without addressing spending patterns, emergency savings gaps, or income volatility. A practical long-term move is to build a small emergency fund while paying down the transferred balance, even if it starts modestly. The goal is to reduce the chance that an unexpected expense ends up back on a credit card. Another habit is to track fixed and variable expenses with enough detail to spot recurring overspending. That does not require perfection; it requires awareness and small adjustments that compound over time. If you rely on credit for basic expenses, the right solution may include renegotiating bills, increasing income, or reducing commitments, not just moving balances around.

It also helps to define what “credit card success” looks like after the promotional period. For some, it means using credit only for expenses that can be paid in full each month. For others, it means keeping one low-fee card for predictable bills to maintain account activity while avoiding discretionary spending on credit. If you keep multiple cards, consider setting spending limits per category or using separate accounts for different purposes. Another long-term strategy is to review card terms annually: interest rates, fees, and any changes to rewards. If you notice that you are repeatedly seeking new promotional offers, it may indicate that the budget is consistently short. In that case, a structured payoff plan, professional credit counseling, or a fixed-rate consolidation loan could provide more stability. The best outcome is not just a paid-off balance; it is a financial system that makes high-interest revolving debt unlikely to return. If you’re looking for 0 interest and balance transfer credit cards, this is your best choice.

Final thoughts on using promotional credit wisely

Choosing and using 0 interest and balance transfer credit cards can be financially powerful when the decision is based on total cost, a realistic payoff schedule, and disciplined spending. The strongest results come from treating the promotional period as a fixed deadline, transferring only what you can reasonably eliminate before the intro APR expires, and automating payments at a level that steadily reduces principal. It also helps to minimize complexity by avoiding new purchases on the transfer card and by keeping careful track of transfer posting dates, fees, and promotional end dates. When the plan is clear and consistent, the interest savings can be substantial, and the psychological boost of watching a balance fall quickly can reinforce better habits.

The key is remembering that 0 interest and balance transfer credit cards are not a permanent interest rate, and they are not a substitute for a sustainable budget. They are a short-term tool designed to give your payments more impact, provided you maintain on-time payments and complete payoff within the promotional window. If your situation fits that structure—high-interest debt, stable income, and a commitment to stop adding new balances—the right offer can accelerate debt freedom. If the timeline is too tight or spending is still unstable, a different consolidation method may be safer even if it costs more. Used with intention and follow-through, 0 interest and balance transfer credit cards can turn expensive revolving debt into a manageable, time-bound project with a clear finish line.

Watch the demonstration video

This video explains how 0% interest and balance transfer credit cards work, including how introductory APR periods can help you pay down debt faster. You’ll learn what fees and deadlines to watch for, how to compare offers, and tips for using these cards responsibly to avoid interest charges once the promo ends. If you’re looking for 0 interest and balance transfer credit cards, this is your best choice.

Summary

In summary, “0 interest and balance transfer credit cards” is a crucial topic that deserves thoughtful consideration. We hope this article has provided you with a comprehensive understanding to help you make better decisions.

Frequently Asked Questions

What is a 0% interest credit card?

A 0% APR credit card gives you a limited introductory period with no interest on purchases, balance transfers, or both—making **0 interest and balance transfer credit cards** a smart option if you want to save on interest while you pay down what you owe. Once the promotional window ends, the card’s standard APR kicks in.

How do 0% balance transfer credit cards work?

You move existing debt from another card/loan to the new card, often paying a one-time transfer fee, and pay 0% interest during the promo period if you make at least the minimum payments on time. If you’re looking for 0 interest and balance transfer credit cards, this is your best choice.

What fees should I expect with a balance transfer?

Most **0 interest and balance transfer credit cards** still come with a balance transfer fee—typically around 3%–5% of the amount you move over. On top of that, you could run into annual fees or late payment fees, and once the promotional period ends, a higher APR may kick in.

Will a balance transfer affect my credit score?

It can affect your credit in a few ways: when you apply for **0 interest and balance transfer credit cards**, you may see a small, temporary score dip due to the hard inquiry. However, if the new credit line helps lower your overall credit utilization, it can actually support your score over time. Just be careful—missing payments or running the new card up to its limit can quickly damage your credit.

Can I transfer a balance between cards from the same bank?

Usually no—most issuers don’t allow transfers between accounts they issue. You typically must transfer from a different lender.

How do I avoid paying interest after the 0% period ends?

Pay the transferred balance in full before the promo expires, make every payment on time, and avoid new purchases on the card unless they also have 0% APR and you can pay them off. If you’re looking for 0 interest and balance transfer credit cards, this is your best choice.

📢 Looking for more info about 0 interest and balance transfer credit cards? Follow Our Site for updates and tips!

Trusted External Sources

- What are the best credit cards to transfer all credit card balance from …

Jun 17, 2026 … Wells Fargo Reflect Card – No SUB. Offers 0% APR for the first 21 months on purchases and balance transfers made in the first 120 days after … If you’re looking for 0 interest and balance transfer credit cards, this is your best choice.

- Balance Transfer Credit Cards | Wells Fargo

Take advantage of a 0% introductory APR for 21 months from account opening on purchases and eligible balance transfers—an excellent option if you’re comparing **0 interest and balance transfer credit cards**. After the intro period ends, a variable APR of 17.49%, 23.99%, or 28.24% applies, depending on your creditworthiness.

- Balance Transfer Credit Cards: Compare Offers | Chase.com

Enjoy a **0% intro APR for 15 months** from account opening on both purchases and balance transfers. Once the introductory period ends, a **variable APR of 18.24%–27.74%** applies. If you’re comparing **0 interest and balance transfer credit cards**, this offer can be a strong option for saving on interest while you pay down transferred balances or finance new purchases.

- Best Balance Transfer Cards for May 2026 – Intuit Credit Karma

The Wells Fargo Reflect® Card stands out among **0 interest and balance transfer credit cards**, offering a 0% introductory APR for 21 months on purchases and on balance transfers made within 120 days of opening your account.

- Balance Transfer Credit Cards – Mastercard

Balance Transfer Credit Cards ; Citi Strata℠ Card. Citi Strata℠ Card · 0% Intro APR for 15 months on purchases. · 0% Intro APR for 15 months on balance transfers. If you’re looking for 0 interest and balance transfer credit cards, this is your best choice.