A practical checklist when buying a house starts with money, but not in the vague “how much can I spend” sense. The first step is defining a budget that reflects your lifestyle, your risk tolerance, and the real monthly cost of ownership. A lender may pre-approve a number that feels flattering, yet that number often assumes you are comfortable stretching your debt-to-income ratio to the upper limit. Instead, calculate a target monthly payment that still leaves room for savings, childcare, travel, hobbies, and emergency repairs. Include principal and interest, property taxes, homeowner’s insurance, and any HOA dues. Then stress-test that number: imagine a temporary income dip, a car replacement, or a medical expense. If the payment would force you to rely on credit cards, the budget is too high. This part of the checklist when buying a house also includes your down payment strategy and closing costs. Closing costs can be significant, and underestimating them can lead to last-minute scrambling or a smaller cash cushion after closing. A strong plan accounts for moving costs, initial furnishings, deposits for utilities, and a reserve fund for the first year of ownership.

Table of Contents

- My Personal Experience

- Setting Your Budget and Defining “Must-Haves”

- Mortgage Readiness, Pre-Approval, and Rate Planning

- Choosing the Right Location and Evaluating Neighborhood Fit

- Finding the Right Team: Agent, Lender, and Specialist Support

- Touring Homes: A Room-by-Room and Systems-Based Approach

- Offer Strategy, Contingencies, and Negotiation Priorities

- Home Inspection: What to Check and How to Interpret Findings

- Expert Insight

- Appraisal, Title, and Legal Due Diligence

- Insurance Planning and Risk Management

- Closing Costs, Final Walkthrough, and Document Review

- Move-In Planning, Immediate Maintenance, and First-Year Priorities

- Resale Considerations and Long-Term Value Protection

- Final Review: A Practical Checklist Mindset Before You Commit

- Watch the demonstration video

- Frequently Asked Questions

- Trusted External Sources

My Personal Experience

When I bought my first house, I thought I could just “feel it out,” but I quickly learned I needed a checklist to keep my emotions in check. I started with the basics—roof age, HVAC, water heater, and any signs of moisture in the basement—because those were the expensive surprises I couldn’t afford. During the showing I tested outlets, ran the faucets, flushed toilets, and opened every window, which felt awkward but saved me from missing obvious issues. I also checked the neighborhood at different times of day, listened for traffic noise, and looked at how water drained after a rain. Before making an offer, I pulled the property tax history, asked for utility bills, and made sure the inspection included the sewer line. By the time we closed, I didn’t feel like I’d found a “perfect” house—I felt like I’d found a house I understood. If you’re looking for checklist when buying a house, this is your best choice.

Setting Your Budget and Defining “Must-Haves”

A practical checklist when buying a house starts with money, but not in the vague “how much can I spend” sense. The first step is defining a budget that reflects your lifestyle, your risk tolerance, and the real monthly cost of ownership. A lender may pre-approve a number that feels flattering, yet that number often assumes you are comfortable stretching your debt-to-income ratio to the upper limit. Instead, calculate a target monthly payment that still leaves room for savings, childcare, travel, hobbies, and emergency repairs. Include principal and interest, property taxes, homeowner’s insurance, and any HOA dues. Then stress-test that number: imagine a temporary income dip, a car replacement, or a medical expense. If the payment would force you to rely on credit cards, the budget is too high. This part of the checklist when buying a house also includes your down payment strategy and closing costs. Closing costs can be significant, and underestimating them can lead to last-minute scrambling or a smaller cash cushion after closing. A strong plan accounts for moving costs, initial furnishings, deposits for utilities, and a reserve fund for the first year of ownership.

Beyond the numbers, define what you truly need versus what would be nice. “Must-haves” should be functional and long-term: number of bedrooms, a safe commute, school district priorities, accessibility needs, and whether you need a dedicated office. “Nice-to-haves” might include a pool, a gourmet kitchen, or a large backyard, but these should not compromise your core budget or location. Consider how your needs may change over five to ten years—remote work policies, family plans, aging parents, or hobbies that require space. This stage is also where you rank trade-offs: would you accept an older kitchen for a better neighborhood, or a smaller home for a shorter commute? Write down your top five non-negotiables and your top five flexible items. That written list becomes a reference point when emotions run high during showings. If you follow this step carefully, the rest of the checklist when buying a house becomes clearer, because every property can be evaluated against a consistent standard rather than impulse.

Mortgage Readiness, Pre-Approval, and Rate Planning

A thorough checklist when buying a house includes preparing your financing before you fall in love with a property. Pre-approval is not just a letter; it is a process that reveals what a lender is willing to offer based on your credit profile, income, assets, and debts. Start by reviewing your credit reports for errors, paying down revolving balances, and avoiding new credit inquiries. Small changes can meaningfully affect your rate, and over the life of a mortgage, even a fraction of a percent can translate into thousands of dollars. Gather documents early: pay stubs, W-2s, tax returns, bank statements, and proof of any additional income. If you are self-employed, expect deeper documentation and plan for extra time. Also consider the type of loan that fits your situation—conventional, FHA, VA, USDA, or a jumbo loan—because each has different down payment rules, mortgage insurance requirements, and appraisal standards. A key financing item on any checklist when buying a house is understanding how your rate could change with points, term length, and your chosen loan product.

Rate planning matters because the “best” mortgage depends on how long you expect to stay and how you manage cash. Some buyers prefer a slightly higher rate with fewer upfront fees to preserve liquidity for renovations and emergencies. Others buy points to reduce the rate if they expect to remain in the home long-term. Ask lenders for a Loan Estimate and compare the APR, not just the interest rate, because the APR reflects many of the costs that show up at closing. Also factor in insurance and property taxes, which can push your monthly payment higher than a simple principal-and-interest estimate. Consider whether you want an escrow account and how that will affect your cash flow. If you are shopping during volatile rate periods, discuss lock options and lock extensions. A solid checklist when buying a house also includes confirming how quickly your lender can close, which can influence the strength of your offer in competitive markets. Finally, keep your financial profile stable: do not switch jobs, make large unexplained deposits, or buy big-ticket items on credit while under contract, because underwriting is designed to detect changes that could increase risk.

Choosing the Right Location and Evaluating Neighborhood Fit

Location is often the factor you cannot change, so the checklist when buying a house should treat neighborhood evaluation as a central task, not an afterthought. Start with a map-based approach: identify commute routes, public transit access, traffic patterns, and proximity to essential services like groceries, healthcare, childcare, and parks. Then go deeper than convenience. Spend time in the area at different hours—weekday mornings, evenings, and weekends—to observe noise levels, street parking, lighting, and general activity. If you are sensitive to sound, check for nearby highways, train lines, flight paths, or popular nightlife corridors. If you value walkability, test it: walk from the property to places you would actually use and note sidewalk continuity and road crossings. A good checklist when buying a house also includes evaluating environmental and climate factors such as flood zones, wildfire risk, and stormwater drainage patterns, which can affect insurance costs and long-term safety.

Neighborhood fit includes social and financial considerations. Review local zoning and future development plans to understand what could change nearby. A vacant lot might become a shopping center, or a quiet street might become a busier connector road. Look into property tax trends and whether the municipality has pending assessments that could raise costs. If schools matter, research more than rankings; consider programs, class sizes, and boundaries that might shift. Also examine community factors that influence quality of life: access to community centers, libraries, trails, and local events. For financial stability, compare recent sale prices and the pace of listings to gauge market health. If you plan to rent out part of the home later, confirm rental restrictions, licensing rules, and HOA policies. This is where the checklist when buying a house should push you to verify assumptions, not rely on a quick drive-by. When you choose a location that matches your daily routines and future goals, you reduce the risk of buyer’s remorse and improve the likelihood that the home will serve you well for years.

Finding the Right Team: Agent, Lender, and Specialist Support

A reliable checklist when buying a house includes assembling a team that protects your interests and reduces costly mistakes. A skilled real estate agent should do more than unlock doors; they should help you interpret market data, craft competitive offers, and anticipate red flags in disclosures and inspection findings. Interview agents and ask about their experience in your target neighborhoods, their typical response times, and how they handle multiple-offer situations. Request examples of recent transactions similar to what you want, including how they negotiated repairs or credits. Your lender is equally important, because delays and miscommunication can jeopardize a deal. Choose a lender who provides clear timelines, explains fees without evasion, and can deliver a pre-approval that listing agents trust. If you are comparing lenders, ask who will actually handle your file day to day and how underwriting is structured. A strong checklist when buying a house prompts you to treat vendor selection as risk management, not just convenience.

Beyond agent and lender, consider specialists who may be necessary depending on the property. A real estate attorney may be beneficial in states where attorneys are standard, or if you are dealing with unique title issues, estates, or complex contingencies. A reputable home inspector is non-negotiable, but you may also need a sewer scope specialist, chimney inspector, structural engineer, or pest inspector depending on the home’s age and features. If the property has a well or septic system, plan for specialized testing. For condos or homes in managed communities, you may need help reviewing HOA documents, budgets, and reserve studies. Your checklist when buying a house should include verifying that these professionals are licensed, insured, and independent—especially inspectors, who should not be pressured to “go easy” to keep referrals. The goal is not to create conflict; it is to ensure you are making a high-stakes purchase with clear information. A well-chosen team helps you understand what is normal wear and tear, what is a real defect, and what should be addressed before you commit.

Touring Homes: A Room-by-Room and Systems-Based Approach

Showings can feel fast and emotional, so the checklist when buying a house should guide you through a consistent evaluation each time. Start outside: observe the roofline, gutters, grading, driveway condition, and signs of water pooling near the foundation. Look for cracks in exterior walls, peeling paint, and wood rot around trim and windows. Inside, scan for uneven floors, sticking doors, and cracks that might indicate settling or structural movement. Pay attention to odors, because persistent musty smells can suggest moisture issues. During tours, test simple items: run faucets, flush toilets, open and close windows, and check for adequate water pressure. Look at the electrical panel if accessible and note whether outlets appear updated. A disciplined checklist when buying a house helps you avoid getting distracted by staging, trendy decor, or a fresh coat of paint that hides deeper issues.

Also evaluate the home as a system rather than a collection of rooms. Ask about the age and service history of the HVAC, water heater, roof, and major appliances. Check the location of the main water shutoff and the electrical shutoff; knowing where these are can be crucial in an emergency. Consider insulation and ventilation: are there signs of condensation on windows, or are bathrooms lacking exhaust fans? Look for evidence of past leaks under sinks, around toilets, and near ceilings. If the home has a basement or crawl space, inspect for moisture, efflorescence on walls, sump pump condition, and proper vapor barriers. Think about layout functionality: can furniture fit, is there enough storage, and does the flow match your day-to-day life? A checklist when buying a house should also include noting natural light, noise transmission between rooms, and cell reception. Take photos and notes after each showing, because multiple homes can blur together quickly. By using a repeatable process, you build confidence that your final choice is based on facts and fit rather than the adrenaline of the moment.

Offer Strategy, Contingencies, and Negotiation Priorities

Writing an offer is where a checklist when buying a house becomes a tactical tool. Price matters, but so do terms. Review comparable sales with your agent to understand fair market value and the likely appraisal range. Consider how long the home has been on the market, the number of offers expected, and the seller’s timeline. A strong offer balances competitiveness with protection. Contingencies—inspection, appraisal, financing, and sometimes sale of another home—are your safety valves. Waiving protections can make an offer more attractive, but it increases your risk, especially if you do not have cash reserves. If you are in a competitive market, you can sometimes strengthen your offer without reckless concessions by offering flexible closing dates, a larger earnest money deposit, or a shorter inspection period while keeping the inspection contingency intact. The checklist when buying a house should prompt you to ask what you are willing to compromise on and what you are not, before negotiations begin.

Negotiation priorities should be anchored in your budget and your risk tolerance. If inspection reveals issues, decide whether you prefer repairs, a credit, or a price reduction. Credits can be helpful because they allow you to choose your own contractors, but they may be limited by lender rules and closing cost caps. Repairs done by the seller can be convenient, but quality varies, and rushed work can create future problems. For appraisal issues, decide in advance whether you can cover an appraisal gap with cash or whether you need the price adjusted. Also consider including language about fixtures, appliances, and any personal property you want to remain. Clarify who pays for what: title insurance, transfer taxes, HOA fees, and home warranties if applicable. A detailed checklist when buying a house includes reviewing deadlines for contingencies and ensuring you can meet them, because missing a deadline can weaken your position or put your earnest money at risk. The goal is to secure a contract that protects you while still being realistic for the seller, setting the stage for a smoother path to closing.

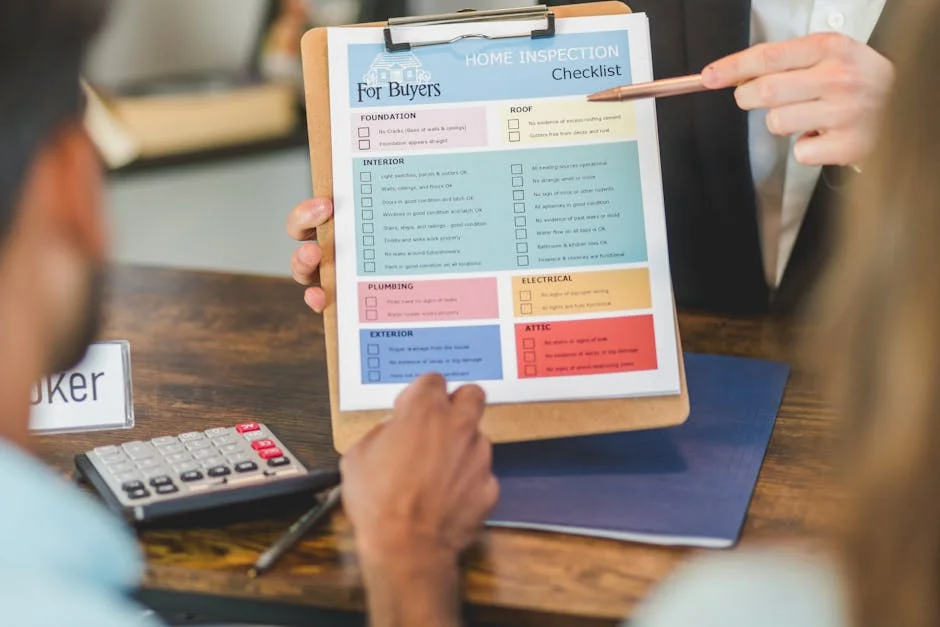

Home Inspection: What to Check and How to Interpret Findings

A home inspection is a core checkpoint on any checklist when buying a house, but the value depends on how you approach it. Attend the inspection if possible and treat it as an educational walkthrough. Ask the inspector to explain major systems, maintenance routines, and the difference between cosmetic issues and functional defects. The report will often be long and can feel alarming because it documents nearly everything. Focus on items that affect safety, structure, water intrusion, and expensive systems like roofing, HVAC, plumbing, and electrical. Look for patterns: multiple signs of moisture in different areas may indicate broader drainage or ventilation problems. Pay attention to foundation concerns, attic ventilation, and evidence of pests or wood-destroying organisms. If the home is older, expect some outdated components; the key is whether they are serviceable, safe, and priced into the deal. A checklist when buying a house should include planning time to get specialist quotes if the inspector flags issues that require further evaluation.

Expert Insight

Verify the home’s true condition before negotiating: review the seller’s disclosures, hire an independent inspector, and request specialist checks (roof, foundation, sewer scope) if any red flags appear. Use the inspection report to prioritize safety and major systems, then ask for repairs, credits, or a price adjustment based on documented findings. If you’re looking for checklist when buying a house, this is your best choice.

Confirm the numbers and the neighborhood fit: get a written loan estimate, calculate total monthly costs (mortgage, taxes, insurance, HOA, utilities, maintenance), and keep a cash buffer for immediate repairs. Research comparable sales, check flood/fire risk and zoning, and visit the area at different times of day to assess noise, traffic, and parking. If you’re looking for checklist when buying a house, this is your best choice.

Interpreting findings is where buyers often make mistakes. Not every defect should trigger a demand for repairs; some are normal maintenance that any homeowner will face. Prioritize items that could worsen quickly, cause hidden damage, or create insurance and financing problems. Electrical hazards, active leaks, mold-like conditions, and unsafe heating equipment deserve immediate attention. For structural concerns, consult a licensed structural engineer rather than relying solely on general inspection notes. For sewer lines, a sewer scope can reveal root intrusion or collapsed sections that are expensive to fix. For fireplaces, a chimney inspection may uncover creosote buildup or liner issues. Your checklist when buying a house should include documenting your repair requests clearly and keeping expectations reasonable. Sellers are more likely to respond positively to a focused list of significant issues than a long list of minor items like loose doorknobs. Also consider the home’s age and renovation history; a recently flipped home can hide shortcuts, so inspect carefully. When you use inspection results to make informed decisions—not emotional reactions—you protect your investment and reduce the chance of costly surprises after move-in.

Appraisal, Title, and Legal Due Diligence

After you are under contract, the checklist when buying a house shifts toward verification. The appraisal protects the lender by confirming the property’s value relative to the loan amount, but it also protects you from overpaying in many scenarios. If the appraisal comes in low, you may need to renegotiate, bring additional cash, or reconsider the deal. Prepare by understanding what features drive value in your area, and ensure your agent provides relevant comparable sales to the appraiser when appropriate. However, appraisals are not the same as inspections; they do not deeply evaluate condition. That is why the appraisal should sit alongside, not replace, your inspection and due diligence steps. A complete checklist when buying a house includes monitoring appraisal timelines and ensuring the lender has what they need to avoid delays.

| Checklist Area | What to Check | Why It Matters |

|---|---|---|

| Finances & Affordability | Pre-approval, total monthly costs (mortgage, taxes, insurance, HOA), closing costs, emergency fund | Prevents budget surprises and ensures you can sustain payments beyond the purchase price |

| Property Condition | Roof, foundation, plumbing/electrical, HVAC age, water damage/mold, inspection report items | Helps avoid costly repairs and strengthens your negotiating position |

| Location & Legal | Neighborhood safety, schools/commute, future development, title search, zoning, permits, flood risk | Protects long-term value and reduces the risk of ownership or resale complications |

Title and legal due diligence are equally critical. Title work confirms the seller has the right to transfer ownership and that there are no liens, disputes, or encumbrances that could affect you. Review the title commitment carefully and ask questions about easements, shared driveways, access rights, and any recorded restrictions. If the property is part of an HOA, review bylaws, rules, financial statements, and reserve funding to gauge whether special assessments may be likely. Confirm property boundaries if there is any uncertainty, and consider a survey, especially for large lots, rural properties, or homes with fences and outbuildings. Your checklist when buying a house should include verifying that permits were obtained for major renovations, because unpermitted work can create safety issues and complicate future resale. Also check whether the property is in a flood zone and what that means for required insurance. These steps can feel tedious, but they prevent painful legal and financial problems that are far harder to fix after closing.

Insurance Planning and Risk Management

Insurance is often underestimated, so a checklist when buying a house should treat it as a planning category, not a last-minute checkbox. Start shopping early, because some properties are harder to insure due to roof age, claims history, location risk, or outdated systems. Request quotes from multiple carriers and compare not only price but coverage details: dwelling coverage, personal property, loss of use, liability, and deductibles. Understand whether your policy covers replacement cost or actual cash value. In areas prone to flooding, hurricanes, earthquakes, or wildfires, additional policies may be required or strongly recommended. Mortgage lenders may require certain coverages, but lender minimums are not necessarily aligned with your real risk exposure. A strong checklist when buying a house includes confirming that the insurance policy’s effective date matches your closing date so there is no coverage gap.

Risk management also includes reducing future premiums and preventing claims. Ask about discounts for security systems, updated roofs, impact-resistant materials, and bundled auto policies. Consider the true cost of a high deductible: it lowers premiums but increases out-of-pocket exposure if something goes wrong. If the home has features like a trampoline, pool, or certain dog breeds, discuss liability implications. For older homes, check whether the insurer requires updates to electrical panels, plumbing, or heating systems. If the property has a history of claims, ask for details and consider what that indicates about maintenance and risk. Also factor in warranty decisions: a home warranty may help with certain appliance and system failures, but coverage can be limited and service quality varies. The checklist when buying a house should encourage you to read policy exclusions, not just skim the declarations page. When insurance is planned thoughtfully, you avoid unpleasant surprises at closing and reduce the chance of discovering after move-in that your dream home is expensive or difficult to protect.

Closing Costs, Final Walkthrough, and Document Review

As closing approaches, the checklist when buying a house becomes detail-heavy, and that is exactly when many buyers are fatigued. Closing costs typically include lender fees, appraisal fees, title services, recording fees, prepaid taxes and insurance, and escrow reserves. Request a Closing Disclosure in advance and compare it to your Loan Estimate to spot unexpected changes. Some costs can shift legitimately, but you should understand why. Verify the interest rate, loan term, projected payments, and whether the loan includes mortgage insurance. Confirm prorations for property taxes and HOA dues, and ask how utilities and assessments are handled. Also plan the logistics of bringing funds to closing, usually via wire transfer, and confirm instructions through a trusted channel to avoid wire fraud. A careful checklist when buying a house includes calling the title company using a verified number, not one provided in an email, before sending money.

The final walkthrough is your last chance to confirm the property’s condition and that agreed-upon repairs were completed. Walk through with your contract and repair addendum in hand. Test lights, outlets, faucets, toilets, HVAC operation, and garage doors. Confirm that appliances included in the sale are present and functional. Check that the home is empty of the seller’s belongings unless otherwise agreed, and that trash and debris are removed. Look for new damage from moving out, such as scratched floors or holes in walls. If repairs were required, request receipts and verify workmanship visually. Document concerns immediately and notify your agent before closing. Your checklist when buying a house should also include reviewing the deed, ensuring names are spelled correctly, and understanding any final documents you sign. This is also the time to confirm you will receive keys, garage remotes, mailbox keys, and any access codes. When you treat closing as a verification process rather than a formality, you reduce the risk of inheriting problems that should have been addressed before ownership transfers.

Move-In Planning, Immediate Maintenance, and First-Year Priorities

The checklist when buying a house does not end when you get the keys; it evolves into a move-in and stabilization plan. Start with safety and utilities. Change exterior door locks, reprogram garage door openers, and update security codes. Confirm smoke detectors and carbon monoxide detectors are installed and functioning, and replace batteries even if they seem fine. Locate the main water shutoff, gas shutoff, and electrical panel and label circuits if needed. Set up utilities and confirm billing transfers. Then address immediate maintenance that prevents damage: replace HVAC filters, clean dryer vents, check gutters, and inspect caulking around tubs and sinks. If the home has a sump pump, test it. If it has irrigation, check for leaks and set a schedule that matches local regulations. A strong checklist when buying a house includes creating a simple home maintenance calendar, because small routine tasks can prevent large repair bills.

Financially, plan for the first year to be more expensive than expected. Even well-maintained homes often require purchases like ladders, lawn equipment, window coverings, and basic tools. Track your initial expenses and rebuild your emergency fund if closing costs reduced it. Review your property tax assessment after purchase; sometimes assessments change after a sale, and that can increase your monthly escrow amount later. If you plan renovations, prioritize projects that improve safety, efficiency, and durability before purely cosmetic upgrades. Address moisture control, insulation, and mechanical updates first, because these affect comfort and long-term costs. Keep a folder with warranties, manuals, inspection reports, and contractor receipts; this documentation helps with maintenance and supports resale value later. Also take time to understand your neighborhood: meet neighbors, learn trash and recycling schedules, and identify local service providers. By treating the first year as an intentional phase, you turn the checklist when buying a house into a sustainable plan for ownership rather than a stressful sprint that ends at closing.

Resale Considerations and Long-Term Value Protection

Even if you plan to stay for years, a smart checklist when buying a house includes thinking about resale, because life changes quickly. Evaluate whether the home has features that tend to hold value in your market: functional layout, adequate bedroom count, reasonable commute access, and a neighborhood with stable demand. Be cautious with properties that have highly unique designs, unusual lot conditions, or location drawbacks that most buyers would notice immediately, such as backing to a noisy road. Also consider how future improvements will be perceived. Over-improving for the neighborhood can be a financial trap if you spend far more than nearby homes support. Instead, focus on upgrades that broaden buyer appeal and reduce future objections: roof replacement when needed, HVAC modernization, energy-efficient windows, updated electrical capacity, and well-documented moisture prevention. A checklist when buying a house should include checking whether additions or conversions were permitted, because unpermitted spaces can complicate appraisals and sales later.

Protecting long-term value is also about consistent care and documentation. Schedule periodic inspections of key systems, especially roofs, chimneys, and HVAC. Keep records of service visits, repairs, and upgrades, and store them in a digital folder. Buyers and appraisers often respond positively to a home with a clear maintenance history. Pay attention to landscaping and drainage; curb appeal matters, but proper grading and water management matter even more because they protect the foundation. If your home is in an HOA, stay engaged enough to understand budget health and upcoming projects, since special assessments can affect marketability. Also monitor insurance costs and coverage adequacy as rebuilding costs rise. Finally, be mindful of how you personalize the home; bold, highly specific design choices can be fun, but if resale is a concern, balance personality with flexibility. The checklist when buying a house becomes truly valuable when it helps you buy with the future in mind, not just the excitement of move-in day.

Final Review: A Practical Checklist Mindset Before You Commit

A successful purchase comes from consistent decision-making more than perfect timing, and the best way to stay consistent is to treat every step as part of a single system. Review your priorities: budget comfort, neighborhood fit, property condition, and financing stability. Re-check the documents that matter most, including disclosures, inspection resolutions, title details, and insurance coverage. Confirm that you understand what you are buying and what you are responsible for immediately after closing. If something feels unclear, press for clarity rather than hoping it will work out. Emotional momentum can push buyers to ignore warning signs, so pause and compare the home against your written requirements and your realistic monthly cost. Also confirm your timeline: moving logistics, work schedules, school transitions, and contractor availability if repairs or renovations are planned. A disciplined approach reduces stress because it replaces guesswork with verification. If you’re looking for checklist when buying a house, this is your best choice.

Most importantly, keep the checklist when buying a house active through the final signatures and beyond. Ensure funds are transferred safely, the final walkthrough matches the agreement, and your post-closing plan is ready: locks changed, utilities confirmed, and a maintenance schedule started. The purchase is not only a transaction; it is the beginning of ownership responsibilities that affect your finances and daily life. When you rely on a checklist when buying a house as a living tool—one that covers budget, financing, location, inspections, legal details, insurance, and long-term value—you give yourself the best chance to buy confidently and settle in without regret.

Watch the demonstration video

This video walks you through a practical checklist for buying a house, from setting a realistic budget and getting pre-approved to evaluating neighborhoods, inspecting the property, and reviewing key documents. You’ll learn what to look for during showings, which costs to plan for, and how to avoid common mistakes before making an offer. If you’re looking for checklist when buying a house, this is your best choice.

Summary

In summary, “checklist when buying a house” is a crucial topic that deserves thoughtful consideration. We hope this article has provided you with a comprehensive understanding to help you make better decisions.

Frequently Asked Questions

What should I confirm about my budget before house hunting?

Get mortgage pre-approval, estimate total monthly cost (PITI, HOA, utilities), plan for closing costs, and keep a repair/emergency reserve.

What documents should I review before making an offer?

Seller disclosures, recent comparable sales, HOA rules/fees (if any), preliminary title report, and any available permits or renovation records.

What inspections should be on my checklist?

Schedule a general home inspection, then bring in any specialists your property or region may require—such as a roofer, sewer scope technician, HVAC professional, electrician, foundation expert, pest inspector, or radon and mold tester. It’s a smart item to include on your **checklist when buying a house** to help you spot issues early and budget with confidence.

What should I check about the neighborhood and location?

When using a **checklist when buying a house**, be sure to weigh everyday realities like your commute and public transit access, nearby school options, local crime and noise levels, flood or fire risk, any future development planned for the area, and how close you’ll be to essentials such as groceries and healthcare.

What financial and legal checks should I do during escrow?

Before you finalize your purchase, use a **checklist when buying a house** to make sure the title is clear, property taxes are accurate, and insurance quotes fit your budget. Review the appraisal carefully, keep a close eye on contingencies and key deadlines, and avoid opening new credit accounts until after closing to prevent last-minute financing issues.

What should I do right before closing and move-in?

Before closing, do a final walkthrough to confirm agreed-upon repairs and that all included items are still in place. Review your closing disclosure carefully, arrange utility transfers ahead of move-in day, and plan to change the locks right away. As part of your **checklist when buying a house**, schedule immediate maintenance like replacing HVAC filters and testing smoke and carbon monoxide detectors.

📢 Looking for more info about checklist when buying a house? Follow Our Site for updates and tips!

Trusted External Sources

- Checklist for first time home buyer : r/RealEstate – Reddit

May 2, 2026 … Comments Section · Get a preapproval from a lender of your choice · Don’t use your credit cards for large purchases/dont apply for new loans, etc. If you’re looking for checklist when buying a house, this is your best choice.

- Checklist for buying your first house – Home – Rocket Mortgage

Aug 11, 2026 … Documents you’ll need for preapproval · Recent pay stubs · W-2 forms · Tax returns · Proof of additional income · Bank statements · Retirement … If you’re looking for checklist when buying a house, this is your best choice.

- Checklist after buying your home : r/FirstTimeHomeBuyer – Reddit

Jul 27, 2026 … Once you’ve closed on your new place, it’s time to tackle a few key tasks to protect your investment. Use this **checklist when buying a house** (and right after you move in): replace HVAC filters and schedule a service visit, clean out gutters and downspouts, and give the entire home a thorough deep clean so you can start fresh.

- Buying a House Checklist: 11 Steps to Homeownership – Own Up

Oct 31, 2026 … Buying a House Checklist: 11 Steps to Homeownership · 1. Do a Financial Checkup · 2. Set a Budget · 3. Talk to Mortgage Lenders and Obtain … If you’re looking for checklist when buying a house, this is your best choice.

- please give me a checklist on how to buy a house. – Reddit

Jan 4, 2026 … Get a property report from the council, knock on neighbors doors and chat. Invite friends and family to the open home. Ask the realtor if you … If you’re looking for checklist when buying a house, this is your best choice.