Choosing a credit card with no balance transfer fees can feel like finding a shortcut through the usual costs that show up when you move debt from one card to another. The phrase sounds simple, but it helps to break down what it typically covers and what it does not. A balance transfer is the process of shifting an existing credit card balance, personal line of credit balance, or sometimes other eligible debt to a new credit card. The new card issuer pays off the old creditor, and you then owe the balance to the new issuer. Many issuers charge a transfer fee—often a percentage of the amount moved—because the bank is effectively purchasing your debt. When a card advertises “no balance transfer fee,” it generally means that the issuer is waiving that percentage-based charge, at least for transfers that meet the card’s terms. That waiver can be valuable because a typical 3% fee on a $10,000 transfer is $300 added to your debt immediately, even before interest. With a no-fee transfer, more of your payment goes to the principal rather than to upfront costs.

Table of Contents

- My Personal Experience

- Understanding What a Credit Card With No Balance Transfer Fees Really Means

- Why Balance Transfer Fees Matter More Than Many People Think

- How Issuers Structure a No-Fee Balance Transfer Offer

- Balancing No Transfer Fees With Intro APR and Ongoing APR

- Eligibility, Credit Score Considerations, and Approval Realities

- Common Fine Print: Time Windows, Transfer Limits, and Exclusions

- Practical Scenarios Where a No-Fee Balance Transfer Can Shine

- Expert Insight

- How to Compare Offers Without Getting Tricked by Marketing

- Step-by-Step: Using a No-Fee Balance Transfer Card Responsibly

- Potential Downsides and Risks to Watch Even When the Transfer Fee Is Zero

- Building a Debt Payoff Strategy That Maximizes the No-Fee Advantage

- Making the Final Choice: When a No-Fee Transfer Card Is the Right Fit

- Watch the demonstration video

- Frequently Asked Questions

- Trusted External Sources

My Personal Experience

When I was trying to get out from under a couple of high-interest cards, I applied for a credit card with no balance transfer fees because I didn’t want to lose money upfront just to move my debt around. I transferred two balances the week I got approved and it was a relief not seeing that usual 3% charge tacked on immediately. The 0% intro APR gave me breathing room, but I still set up automatic payments and made a plan to pay it down before the promo ended. It wasn’t a magic fix, but skipping the transfer fee made the whole move feel worth it and helped me put more of each payment toward the principal instead of extra costs.

Understanding What a Credit Card With No Balance Transfer Fees Really Means

Choosing a credit card with no balance transfer fees can feel like finding a shortcut through the usual costs that show up when you move debt from one card to another. The phrase sounds simple, but it helps to break down what it typically covers and what it does not. A balance transfer is the process of shifting an existing credit card balance, personal line of credit balance, or sometimes other eligible debt to a new credit card. The new card issuer pays off the old creditor, and you then owe the balance to the new issuer. Many issuers charge a transfer fee—often a percentage of the amount moved—because the bank is effectively purchasing your debt. When a card advertises “no balance transfer fee,” it generally means that the issuer is waiving that percentage-based charge, at least for transfers that meet the card’s terms. That waiver can be valuable because a typical 3% fee on a $10,000 transfer is $300 added to your debt immediately, even before interest. With a no-fee transfer, more of your payment goes to the principal rather than to upfront costs.

Even so, “no fee” should not be confused with “no cost.” A credit card with no balance transfer fees may still have interest charges, and it may or may not include a promotional APR period. Some cards pair the fee waiver with a 0% introductory APR for a set number of months, while others remove the fee but keep a standard purchase APR or a reduced transfer APR that starts right away. Timing also matters: some issuers offer no balance transfer fee only for transfers completed within a certain window after account opening, such as the first 60 or 90 days. After that, a fee may apply. Additionally, balance transfers may not include every type of debt; for example, many issuers exclude mortgages, auto loans, student loans, or balances owed to the same bank. Understanding these nuances is essential because the headline benefit can be undermined by fine print. A strong approach is to treat the no-fee feature as one part of a broader cost equation that includes APR, promotional length, credit limit, and repayment plan.

Why Balance Transfer Fees Matter More Than Many People Think

Balance transfer fees are easy to underestimate because they are often presented as a small percentage, and percentages can feel abstract compared to a monthly payment. Yet the fee is typically added to your balance immediately, which means you are paying interest on it unless you pay it off quickly during a promotional period. That is why a credit card with no balance transfer fees can provide a clearer, cleaner path to reducing debt. Consider how quickly a fee compounds the challenge: if you transfer $7,500 with a 4% fee, you start at $7,800. If you were already struggling to make progress, that extra $300 can mean an additional month or two of payments, or it can reduce the effectiveness of a 0% APR window because you have more principal to eliminate before the promotion ends. Eliminating the fee helps ensure that the transfer is actually a step forward rather than a reshuffling of debt with extra cost.

Fees also matter because they can distort how people compare offers. Many consumers focus on the length of a 0% APR promotion and assume that a longer period automatically means a better deal. Sometimes it does, but not always. A shorter promotional period with no transfer fee can beat a longer promotion that charges a high fee, especially if you plan to pay the balance down aggressively. The best comparison is to calculate the total cost: upfront fee, expected interest after the promo ends, and how much you can realistically pay each month. A no-fee transfer can be particularly beneficial when the balance is large, when you are transferring multiple balances at once, or when you may need to do a second transfer later. It is also helpful when you are consolidating debt as part of a broader financial reset, because the absence of a fee reduces the “penalty” for taking action. Still, you should watch for other charges, such as annual fees, late fees, or penalty APR triggers, because these can erase the advantage if you miss payments or carry the balance beyond the promotional terms. If you’re looking for credit card with no balance transfer fees, this is your best choice.

How Issuers Structure a No-Fee Balance Transfer Offer

A credit card with no balance transfer fees is not always “no fee forever” in every scenario; it is usually structured around a specific marketing offer. Many issuers design the deal to attract new customers who have balances elsewhere. The most common structure is a limited-time fee waiver for transfers initiated shortly after account opening. The issuer may require that the transfer request be made within a set timeframe, and sometimes the transfer must also post to the account within that window. Another structure is a permanent no-fee policy, which is less common but can exist in certain product lines or in certain markets. A third structure involves targeted offers: an existing customer might receive a special no-fee balance transfer promotion through email or in the online account portal. These targeted offers can be excellent, but they are also time-sensitive and may apply to specific transfer amounts or APR terms.

It is also important to understand how the transfer itself works operationally. Some issuers allow you to initiate the transfer during the application process, while others require you to wait until the account is approved and active. Processing times can range from a few days to a few weeks. During that processing period, you may still owe minimum payments to the original creditor, and interest may continue to accrue there until the payoff is completed. A no-fee offer does not change that timing reality, so planning is essential. Additionally, issuers may set a maximum transfer amount, often tied to your credit limit, and they may only allow transfers up to a certain percentage of that limit. If your credit limit is lower than expected, you might not be able to move all your balances at once. In that case, the best use of a no-fee transfer is to prioritize high-interest balances first. Understanding the structure helps you avoid surprises and helps you use the offer in a way that actually reduces your total cost of debt. If you’re looking for credit card with no balance transfer fees, this is your best choice.

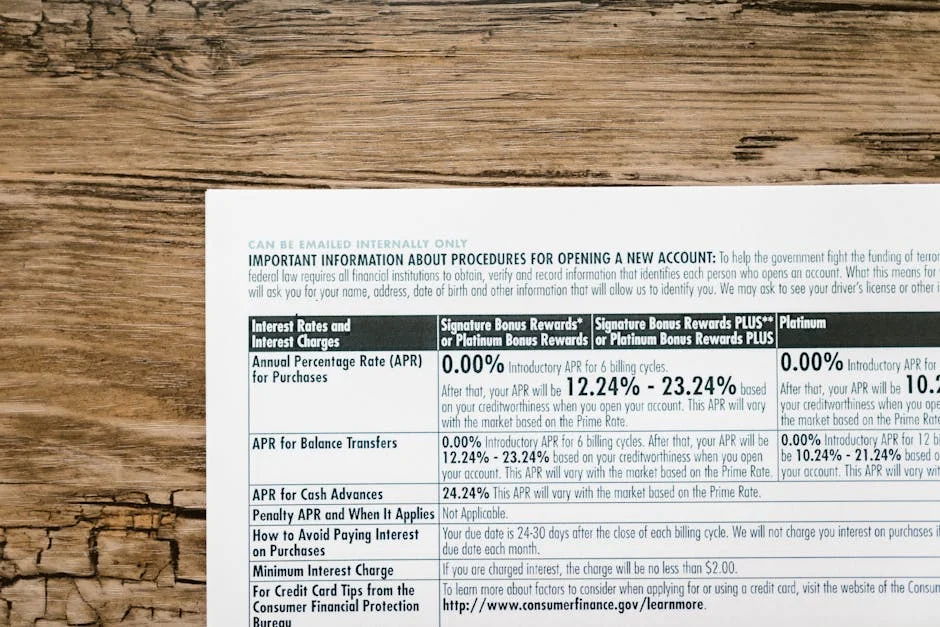

Balancing No Transfer Fees With Intro APR and Ongoing APR

People often search for a credit card with no balance transfer fees because they want to avoid paying extra upfront. That makes sense, but the APR picture matters just as much. Some cards offer a 0% introductory APR on balance transfers for a set period, such as 12, 15, or 18 months. Others may offer a low APR rather than 0%. If there is no promotional APR, then a no-fee transfer can still be useful, but you must compare the new APR to the APR on your existing debt. If your current card charges 24% and the new card charges 18%, you may still save money without paying a fee, but the savings depend on your repayment pace. When comparing, it helps to estimate how much interest you would pay under each option over the time you expect to take to pay off the balance. A fee waiver can tilt the math in your favor, but it cannot compensate for a significantly higher ongoing APR.

Another detail is how purchases are treated while you carry a transferred balance. Many cards apply payments to the lowest APR balance first, which can be problematic if you make new purchases at a higher APR while your transfer sits at 0% or low interest. In that scenario, interest can accumulate on purchases even if you are paying more than the minimum, because your payment may not immediately reduce the purchase balance. For someone using a no-fee transfer card primarily to pay down debt, the simplest approach is often to avoid new purchases on that card until the transferred balance is fully paid. If you need a daily spending card, using a separate card and paying it off each month can keep your balance transfer strategy clean. The goal is to ensure that the no-fee feature leads to real progress, rather than creating a mixed-balance situation where interest charges creep in and slow down payoff. If you’re looking for credit card with no balance transfer fees, this is your best choice.

Eligibility, Credit Score Considerations, and Approval Realities

Finding a credit card with no balance transfer fees is only part of the challenge; approval and credit limit are just as important. Issuers evaluate applicants using credit scores, income, existing debt, and overall credit profile. Even if you qualify, the credit limit you receive determines how much you can transfer. Many people aim to transfer large balances to reduce interest, but if the new limit is smaller than expected, you may only be able to transfer a portion. That can still help if you target the highest-interest balance first, but it may require a more nuanced plan. It is also worth noting that applying for a new card typically results in a hard inquiry, which can temporarily lower your score. For most people, that short-term impact is minor compared to the potential savings from reduced interest and fees, but it is still a factor to consider if you are planning a major loan application soon.

Another reality is that “no balance transfer fee” offers may be concentrated among certain issuers or product categories, and some of them may be targeted to applicants with good to excellent credit. If your credit is fair or rebuilding, you might see fewer true no-fee options, or you may see offers that look attractive but have shorter promotional periods, higher ongoing APR, or additional costs like annual fees. In that case, the best evaluation is still the total cost and the practicality of payoff. It can also help to improve your approval odds by checking prequalification tools when available, keeping credit utilization lower before applying, and ensuring your income and housing payment information are accurate. If you are already carrying high utilization, paying down even a small amount before applying could improve your score and help you qualify for a better limit. The point is not to chase an offer blindly, but to align the product with your current credit profile and your realistic debt payoff timeline. If you’re looking for credit card with no balance transfer fees, this is your best choice.

Common Fine Print: Time Windows, Transfer Limits, and Exclusions

The most frequent disappointment with a credit card with no balance transfer fees comes from overlooked restrictions. A common rule is the “intro window” requirement: you must initiate the transfer within a certain number of days after opening the account. If you miss that window, the issuer may charge the standard transfer fee. Another limitation is the maximum amount you can transfer. Even if your credit limit is $10,000, the issuer might only allow transfers up to $9,000 or less, leaving room for fees (if any) or to manage risk. Some issuers also restrict how many transfers you can initiate or how frequently you can do them. These limitations matter if you plan to consolidate multiple cards, because you might need to stagger transfers or prioritize which balances to move first.

Exclusions can also surprise people. Many issuers will not allow you to transfer a balance from a card issued by the same bank or from an affiliated brand. Some will not allow transfers from certain types of accounts, such as a loan or a line of credit, even if it feels similar to a credit card balance. There can also be minimum transfer amounts, meaning you cannot transfer a very small balance just to take advantage of a promotion. Another critical point is payment allocation and promotional forfeiture. If you make a late payment, some issuers may end the promotional APR and apply a penalty APR, which can be significantly higher. While a no-fee transfer reduces upfront cost, it does not protect you from late fees or penalty terms. Reading the balance transfer section of the card’s terms and conditions is not optional if you want to avoid unpleasant surprises. A careful review helps ensure that the no-fee promise applies to your specific situation and that your payoff plan fits within the rules. If you’re looking for credit card with no balance transfer fees, this is your best choice.

Practical Scenarios Where a No-Fee Balance Transfer Can Shine

A credit card with no balance transfer fees can be particularly effective in a few real-world scenarios. One common situation is when you have a large balance on a high-interest card and you can commit to paying it down quickly. If you can pay $600 per month and you have a $6,000 balance, a 0% period of 12 months could allow you to eliminate the balance without interest, and the absence of a transfer fee means you start at exactly $6,000 instead of $6,180 or more. Another scenario is when you have multiple smaller balances spread across cards with different due dates and interest rates. Consolidating them onto one card can simplify payment management and reduce the risk of missing a due date. If the consolidation also avoids transfer fees, it reduces the cost of simplifying your finances.

| Option | Balance Transfer Fees | Best For |

|---|---|---|

| True $0 Balance Transfer Fee Card | $0 (no intro or ongoing transfer fee) | Moving debt without paying a transfer fee, even if the intro APR is shorter. |

| Intro $0 Fee, Then Standard Fee | $0 during promo window; typically 3%–5% afterward | Transferring quickly within the promo period and paying down debt during an intro APR. |

| Low/No Fee via Credit Union or Promo Offer | Often $0–3% (varies by issuer and offer) | Borrowers who qualify for member deals and want lower costs with competitive APR terms. |

Expert Insight

Compare cards that advertise no balance transfer fees by checking the full fee schedule and the length of any promotional APR. Prioritize offers with a long 0% intro period and confirm whether the no-fee transfer applies to all transfers or only those made within the first 30–60 days. If you’re looking for credit card with no balance transfer fees, this is your best choice.

Before transferring, map out a payoff plan that clears the balance before the promotional rate ends. Set up automatic payments above the minimum and avoid new purchases on the same card if they accrue interest immediately or complicate payment allocation. If you’re looking for credit card with no balance transfer fees, this is your best choice.

No-fee transfers can also help when you are near the end of a promotional period on another card and you still have a remaining balance. Some people “rotate” balances from one promotional offer to another to avoid interest, though this strategy requires discipline, strong credit, and careful timing. A fee-free transfer makes the rotation less expensive, but you should be cautious: repeatedly applying for new credit can affect your score, and if your income or credit profile changes, you might not qualify for the next card when you need it. Another scenario is when you are dealing with a temporary cash flow issue—such as a job transition or an unexpected expense—and you need breathing room to stabilize without adding a fee to your balance. In every scenario, the same principle applies: the no-fee feature works best when paired with a structured payoff plan and a commitment to avoid new high-interest spending on the card. If you’re looking for credit card with no balance transfer fees, this is your best choice.

How to Compare Offers Without Getting Tricked by Marketing

Marketing language can make different cards sound similar, even when the costs are dramatically different. To compare a credit card with no balance transfer fees against other offers, start by listing the key variables: promotional transfer APR, promotional duration, ongoing APR range, annual fee, and any conditions for the fee waiver. If the card has no transfer fee but a shorter promo period, calculate whether you can realistically pay off the balance within that time. If you cannot, estimate what happens after the promotion ends: what APR applies, and how much interest would accumulate if you continue paying at your expected rate. If a competing card charges a fee but offers a longer 0% period, compare the total cost over your payoff horizon, not just the first month. Often, the best deal is the one with the lowest total cost given your specific payment plan.

It also helps to evaluate the “behavioral” fit of the card. Some people benefit most from simplicity: one balance, one due date, one payment. Others need a longer runway because their monthly budget is tight. A no-fee transfer can be a strong choice for someone who can pay aggressively, because the fee savings are immediate. But if your payoff plan requires a longer time, the length of the promotional APR could be more important than the fee. Another marketing trap is focusing on “up to” language. If an offer says “0% intro APR for up to 18 months,” your actual terms may differ depending on the product variant or your credit profile. You should confirm the exact promotional duration and APR that applies to your application. Finally, consider whether the card also offers useful features you might keep long-term, such as rewards on purchases you pay off monthly, or whether it is purely a debt payoff tool you plan to stop using once the balance is gone. If you’re looking for credit card with no balance transfer fees, this is your best choice.

Step-by-Step: Using a No-Fee Balance Transfer Card Responsibly

Using a credit card with no balance transfer fees effectively is less about the application and more about the execution. Start by pulling your current statements and listing each balance, APR, and minimum payment. Decide which balances you want to transfer, usually prioritizing the highest APR first. Once approved, initiate the transfer promptly, especially if the no-fee feature is tied to a limited-time window. Continue making at least the minimum payments on your old cards until you see the transfer post and the old balances are confirmed as paid. This avoids late fees and credit report damage during the processing period. When the transfer completes, set up autopay for at least the minimum on the new card. Missing a payment can trigger late fees and potentially end promotional terms, which can quickly negate the benefit of avoiding a transfer fee.

Next, build a payoff plan that fits the promotional timeline. Divide the transferred balance by the number of months in the intro period to estimate the monthly payment needed to reach zero before interest begins. If the result is too high, consider whether you can increase income, cut expenses, or transfer a smaller amount so you can fully pay it off. Avoid using the card for new purchases unless you are confident you can pay those purchases off immediately and the card’s payment allocation rules will not cause interest to accrue. Many people find it safer to keep the balance transfer card “debt-only” and use a separate card or debit for daily spending. Finally, track progress monthly. If you receive a bonus, tax refund, or other windfall, applying it to the balance can accelerate payoff and reduce the risk of carrying debt beyond the promotional period. The no-fee feature is a strong start, but consistent payments are what turn it into real savings. If you’re looking for credit card with no balance transfer fees, this is your best choice.

Potential Downsides and Risks to Watch Even When the Transfer Fee Is Zero

A credit card with no balance transfer fees can still carry meaningful risks if it encourages complacency. One risk is treating the transfer as a solution rather than a tool. If spending habits remain unchanged, it is easy to run up balances again on the old cards after transferring them, leaving you with more total debt than before. Another risk is relying on the promotional APR without planning for what happens when it ends. If the balance is not paid off in time, the remaining amount may begin accruing interest at a standard rate, which can be high. Some cards do not charge retroactive interest on the transferred balance during a 0% period, but you should still confirm the terms because promotional structures vary. Even without retroactive interest, carrying a large balance beyond the promo can be costly.

There are also credit score considerations. Opening a new account can reduce your average account age, and the hard inquiry can cause a small temporary dip. However, lowering utilization by moving balances can help your score if it reduces the percentage of available credit you are using, especially if you do not close old accounts immediately. Still, there is a psychological risk: a higher total credit limit across cards can tempt additional spending. Another downside is that some no-fee balance transfer cards may not offer strong long-term value once the debt is paid off, such as limited rewards or benefits. That is not necessarily a problem if your goal is debt payoff, but it matters if you want to keep the card long-term. Finally, if you are close to maxing out the new credit limit, it can hurt your utilization on that card and may make it harder to qualify for additional credit if you need it. The best way to manage these risks is to treat the transfer as a structured payoff program, with clear monthly targets and limited new spending. If you’re looking for credit card with no balance transfer fees, this is your best choice.

Building a Debt Payoff Strategy That Maximizes the No-Fee Advantage

To get the most from a credit card with no balance transfer fees, the payoff strategy should be designed around speed, predictability, and behavior change. Start by selecting a monthly payment that is comfortably above the minimum and aligned with your promotional period. If your intro APR lasts 15 months and your balance is $4,500, a simple target is $300 per month to reach zero by the end of the promotion, assuming no new charges. If you can pay $350, you create a buffer for timing issues, statement cycles, or unexpected expenses. It is also helpful to synchronize your payment schedule with your paydays. Some people pay half the target payment every two weeks, which can make the budget easier to manage and can reduce average daily balance if interest applies later. Even with 0% APR, frequent payments can support discipline and reduce the temptation to spend the money elsewhere.

Next, address the behavior that created the debt. A no-fee transfer can reduce costs, but it does not fix a budget gap. If overspending is the issue, create category limits and track them weekly. If irregular income is the issue, build a small buffer fund so you do not rely on credit for basic expenses. If unexpected expenses are the issue, plan for them with sinking funds for car repairs, medical copays, or annual bills. Also consider whether to keep old cards open. Keeping them open can help utilization, but only if you do not use them to accumulate new debt. Some people freeze the cards (literally or figuratively) while they pay down the transfer. Another tactic is to set alerts: balance alerts, due date reminders, and payment confirmations. These small systems reduce the risk of missed payments that could wipe out the benefit of the no-fee feature. When the balance reaches zero, decide whether to keep the card for occasional use and paid-in-full spending or to store it as a backup, depending on its long-term value and your spending habits. If you’re looking for credit card with no balance transfer fees, this is your best choice.

Making the Final Choice: When a No-Fee Transfer Card Is the Right Fit

The best time to choose a credit card with no balance transfer fees is when you have a clear payoff plan and you want to reduce friction costs that slow down progress. If you are motivated to pay down debt within a promotional period, avoiding a transfer fee can be like getting an immediate discount on your debt. It can also be the right fit when you are consolidating multiple balances and want the simplest possible start—no added percentage fee, no inflated principal, and a straightforward path to zero. The no-fee benefit is especially meaningful on larger balances, where even a small percentage fee translates into a sizable dollar amount. It can also be a strong option when you are comparing two similar cards and the only major difference is whether the transfer fee is waived.

At the same time, the right fit depends on details that go beyond the headline. You still need terms you can live with: a promotional APR that matches your payoff timeline, an ongoing APR that will not be punishing if you need extra time, and account features that help you stay on track, such as autopay and alerts. You also need to be honest about spending habits, because moving debt without changing behavior can create a cycle that is harder to escape. If you approach the decision with a full-cost mindset—considering promo length, APR, credit limit, and your monthly payment capacity—the no-fee feature becomes a practical advantage rather than a marketing hook. With the right planning and follow-through, a credit card with no balance transfer fees can be a powerful tool for simplifying repayment, reducing total costs, and reaching a debt-free milestone faster.

Watch the demonstration video

In this video, you’ll learn how credit cards with no balance transfer fees work and when they can help you save money. We’ll cover what “no fee” really means, key terms like introductory APR periods, eligibility requirements, and common pitfalls to avoid so you can choose the right card and pay down debt faster. If you’re looking for credit card with no balance transfer fees, this is your best choice.

Summary

In summary, “credit card with no balance transfer fees” is a crucial topic that deserves thoughtful consideration. We hope this article has provided you with a comprehensive understanding to help you make better decisions.

Frequently Asked Questions

What is a credit card with no balance transfer fees?

A **credit card with no balance transfer fees** lets you move debt from another credit card or loan without paying the usual balance transfer charge—often around **3% to 5%** of the amount you transfer.

Does “no balance transfer fee” mean the transfer is completely free?

Not necessarily—even if the transfer fee is $0 with a **credit card with no balance transfer fees**, you could still end up paying interest if the card doesn’t offer a 0% intro APR, if the promotional period expires, or if you miss a payment.

Do no-fee balance transfer cards usually come with a 0% intro APR?

It depends. Some cards are a **credit card with no balance transfer fees** but still charge a regular APR right away, while others waive the transfer fee and also offer a limited-time 0% intro APR to help you pay down debt faster.

Are there limits on how much I can transfer with a no-fee balance transfer card?

Yes—balance transfers are usually limited by your approved credit limit and may also be capped by your card issuer’s rules. In many cases, you can’t move a balance between cards from the same bank, even if you have a **credit card with no balance transfer fees**.

How long do I have to make a balance transfer to qualify for no fees?

Many promotions only apply if you move your balance within a specific timeframe—often 30 to 60 days after opening the account—so read the fine print and mark the deadline, especially if you’re considering a **credit card with no balance transfer fees**.

Will a balance transfer affect my credit score?

Yes, it can. Opening a new card may cause a small, temporary dip in your score, but it can also lower your credit utilization and help you pay down debt faster over time—especially if you avoid adding new balances. Choosing a **credit card with no balance transfer fees** can make that strategy even more effective by keeping more of your payment going toward the principal instead of upfront costs.

📢 Looking for more info about credit card with no balance transfer fees? Follow Our Site for updates and tips!

Trusted External Sources

- Are there any cards with zero fees for balance transfers? – Reddit

Sep 30, 2026 … Wells Fargo Reflect has 0% APR for 21 months for transfer fees and purchases. It’s currently the best debt elimination card out there. The only … If you’re looking for credit card with no balance transfer fees, this is your best choice.

- Best No Balance Transfer Fee Credit Cards – NerdWallet

As of Dec. 21, 2026, Skyla Credit Union’s Visa Platinum card stands out as a **credit card with no balance transfer fees**—and no annual fee. It also features an introductory 0% APR offer, making it a compelling option if you’re looking to move existing debt and save on extra costs.

- ANY True FREE balance transfers CCs? : r/CreditCards – Reddit

Jun 23, 2026 … The closest one can get is the Navy Federal cashRewards card . It has a 1.99% APR for the first 12 months with no balance transfer fee for … If you’re looking for credit card with no balance transfer fees, this is your best choice.

- What are Credit Cards with No Balance Transfer Fees – Citi.com

As of Oct 7, 2026, some issuers promote introductory balance transfer offers that waive the usual transfer charge—so you can move existing debt over without paying a percentage fee. If you’re comparing options, look for a **credit card with no balance transfer fees**, since that kind of promotion can help you save money upfront while you work on paying down what you owe.

- Are there credit cards with no balance transfer fee? – Reddit

Dec 5, 2026 … I’m currently in the middle of a balance transfer where Wells Fargo offered me 0% APR balance transfer with 0% fees for 15 months. Snapped that … If you’re looking for credit card with no balance transfer fees, this is your best choice.